MGX Minerals Inc. (XMG:CSE; MGXMF:OTCBB) is a rare breed of junior, as it has a staggering 22 ongoing projects, it is CSE listed, works on revolutionary "petrolithium" and zinc air fuel cell tech, has booked no tangible, independently verifiable results yet, but still manages to raise tens of millions of dollars like it's nothing, and keeps producing a true avalanche of news releases because of these 22 projects. When talking to management, there are always plans for even more projects they might go after. Too much? One might think so as progress is slower than projected on several fronts and results are few and far in between, while in the meantime new projects are being added, seemingly creating ever-changing dynamics in a vibrant pool of increasing activity as far as focus and strategy is concerned.

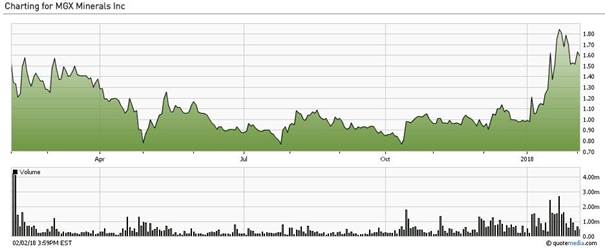

However, this is about to change, as MGX is looking to bring the first 750 bpd wastewater brine plant in Alberta in production within 45 days, and announce the coveted Driftwood PEA results within two weeks. I consider these two projects definitely to be cornerstone value indicators for MGX, and as such both developments will provide important tangible information about current and future value of the company. As investors also seem to get the feeling something is about to evolve, positive sentiment is reflected in the share price lately:

Share price; 1 year time frame

Share price; 1 year time frame

With the two already mentioned catalysts ahead, and the closed $12.9M financing, besides numerous other smaller developments, it looked like a good time to interview CEO Lazerson again on the current state of affairs.

TCI: Thanks, Jared for taking the time again; it will be another, slightly less extensive interview but so many things are happening with your company, it is remarkable. Don't you ever lose oversight?

JL: You are most welcome, and I always enjoy your questioning as it makes me rethink/refocus/reprioritize things as it can be a bit much or unclear for investors at times for sure. My management model on the other hand is very simple: I am the only full-time employee of the company, and I hire freelance experts for every task or project at hand. Therefore, I am not dealing in-depth with all operations myself and delegate a lot of things, but still manage to keep overview in the end as everybody reports to me.

TCI: Lots of mining juniors have part-time teams, but I'm sure this will evolve when revenues start coming in and scale up. Let's discuss the progress on the first actual contract that is in place for Purlucid and MGX.

JL: Sure. It is a contract with a major oil sands company, for a 1,200m3 per day, $45/m3 revenue agreement. Purlucid has to treat the highly toxic wastewater that is present in the resulting steam when producing oil from sands, which goes by injecting steam to liquify the oil from tar sands. Normally this treatment would cost those producers about $100/m3, so this is very interesting for them. This type of high margin contracts is very hard to get, so I view this as an excellent opportunity. There are no direct revenues for MGX; there might be a dividend in the future. MGX recently increased ownership of Purlucid to 51% so it is in control now. When Purlucid becomes more profitable in the future, we will increase ownership further.

TCI: What is the status on the normal waste water treatment projects; this is something special and high margin as we just discussed. Any contracts on the horizon yet?

JL: We don't have any contracts coming up on this subject for now; the system isn't set up for mass handling yet. Notwithstanding this, I still believe this is a big market for Purlucid, as costs of $1-1.5/barrel are 10-25% of existing costs of treating wastewater for oil producers. We will be looking at large contracts in this field next year when the plant has proven itself.

TCI: Talking about oil producers, what is the progress on the O&G assets?

JL: The sight survey for the 3D seismic is done, and we are about to commence the archeologic and paleontologic survey. After this has been completed and approved, a drill permit will be granted; this is anticipated for August this year. MGX is not sure if O&G should be strategic or not; we don't like to be in the O&G business per se. We don't like to sell Paradox either as this asset is very valuable, so Chairman Bruner is looking for partners to bring this further. We would like to start drilling before the end of this year, planned for the end of Q3, 2018.

TCI: You said during the other interview it was an option to sell the treated clean water coming out of the waste water treatment process, depending on each project, do you still think the same about this or are you focusing more? Is the filtration technology able to be applied to other water purification needs as well? An example would be treatment of contaminated water from natural disasters such as the hurricanes that impacted the Caribbean and Texas this past fall? If so, are there any plans in the near term (or in any time frame) to pursue those opportunities?

JL: We are indeed focusing more and more on processing now, so we will avoid trading/selling clean water. We are also not looking into, for example, desalination solutions as they are low margin and are getting away from our core strengths.

TCI: Could you give us a renewed status update on timelines for commercial contracts?

JL: As we discussed, we have our first (and high margin) contract with an oil sands player in place. Regarding the demonstration contracts, 90% is completed, 2 or 3 from 12 are being followed up at the moment. MGX is looking for projects with scale. One of the follow up contracts the company is closing in on is a 5,000 bpd agreement with Chesapeake Oil, which has wastewater containing 200 ppm Li which is very high in wastewater terms. MGX foresees about $3.4M in LCE revenues, and about $7M in water treatment revenues, together generating $6.7M in profits. MGX is still within the demonstration contract on this one, bulk samples are ongoing, more testing has to be done, could take another six months for a decision.

TCI: Has MGX an idea of any hard indicators on all its projects, like actual cost/CF indications, production units, capex for them and how to raise the cash for it, timelines on units production itself?

JL: Costs are all pretty project sensitive, however in general we have a good idea now as much has been tested. Processing cost of 100 ppm Li wastewater is about $1-1.5/barrel, of 1000 ppm Li clean brine is about $0.5-1/barrel. A 1,200m3 wastewater system costs an estimated $3M, a 2,400m3 system about $4.5M. For clean brine a 1,200m3 system would cost an estimated $2M, and a 2,400m3 system about $3-3.5M.

TCI: When exactly are the 750 bpd and 7,500 bpd plants completed, and what caused the delay as these were both supposed to be up and running now?

JL: The 750bpd plant will be finished in March 2018, and this means a six-month delay that was caused by more additional testing. The 7,500 bpd plant will be finished in June, which also means a six-month delay, but this has been caused predominantly by the government grant of $8.2M taking longer, besides more testing. This grant is to pay for equipment for the aforementioned oil sands water handling contract, where this would pay for about 2/3 of the necessary equipment of a 7,000-bpd plant and MGX would pay the balance (about $4.1M). That project is a nice consortium of government, an oil sands producer, our engineering partner Purlucid and a big systems partner to handle control systems, remote monitoring and AI.

MGX paid $1.25M of the $4.1M before December 31, 2018, and the balance will be paid well after the plant is finalized, probably in the last quarter of 2018. When making these payments, MGX also acquires ownership in Purlucid at the same time. After paying $4.1M in full, the company would own 66% of Purlucid.

TCI: As MGX becomes more familiar with the process of producing the machine that extracts Li and treats wastewater, what is the current expected time to produce one unit for deployment, and is that time expected to decrease with economies of scale or by other means?

JL: The end to end manufacturing time is approximately four months, including installation at about six months. Scale is not really affected by this as the systems are modular at this time, whether a system is 1,200 cubic meters or 2,400 cubic meters per day, it doesnt significantly affect the manufacturing time. The way we will accelerate is by manufacturing multiple units at one time.

TCI: What kind of lithium product are you looking to provide through the wastewater treatment/brine systems? During the last interview we discussed the upgrading of a low-grade lithium chloride concentrate into lithium carbonate (LCE).

JL: Yes, part of this is still the case; the plan is to deliver lithium chloride, concentrated to 25-30%, which process of extraction and concentration from start to finish is planned to take 1-2 days. 100% LiCl would generate $6,900/t, and the minimum concentrate accepted by upgraders is 18% so we easily get to that threshold. MGX is no longer planning on upgrading to LCE and sell this ourselves, as major lithium feedstock consumers have indicated to MGX that they are looking for lithium chloride concentrate. Costs are estimated at $2,000/t LiCl for wastewater, and about $1,000/t LiCl for clean brine.

TCI: Are you looking into acquiring clean brine assets, and if so could you mention areas of interest?

JL: At the moment we are actively looking in Chile for new brine assets, and we recently started working together with Kura Geoscience in Chile, as it will be representing us in any local deal we might pursue there. With our method we don't need standard economic grade brines, like 500-600mg/L Li; half of this would be already very interesting.

TCI: Last time we discussed concentration efforts of 67 ppm Li to 1,600 ppm Li, making it rival LatAm grades. What is the status on this?

JL: We managed to concentrate this further to even 5,000 ppm Li at hardly any additional cost as it is a locked cycle concept.

TCI: I am definitely looking forward to further developments in the clean brine space and actual lithium chloride production. Let's have a closer look now at one of your flagship industrial mineral projects, Driftwood Creek.

What is the status of this upcoming Driftwood PEA, and the scheduled timeline on this?

JL: The PEA is almost completed. There have been several changes across the board, in part thanks to extensive test milling. The capex will rise from $60M to $100M, the daily throughput will increase from 400 tpd to 1,100 tpd, total production will increase to 2.7Mt MgO. We have the option to mill it on site, but we could also ship a 25% concentrate across the border for double revenues for magnesium metal. The publication timeline on the PEA will be the end of February 2018.

TCI: Thanks, and according to my schematic DCF model this will result in a slightly lower after-tax NPV5 of about $170M (was $198M) and a significantly lower IRR of about 18% (was 27.6%), but still economic, and much better than far lower grade competitors Nevada Clean Magnesium and West High Yield Resources. As the Driftwood PEA experienced a year delay since we discussed it the very first time, I would like to ask you again if Driftwood still is something the company plans to pursue, or with all other projects developing are you only looking to maximize value and sell it?

JL: No, Driftwood still remains a cornerstone asset and this will stay that way. I am not pleased with the very slow PEA engineering myself, and will probably bring in SRK to do the PFS. MGX is politically well connected, and is looking into bringing in partners to finance capex and get this into production as soon as possible.

TCI: On a sidenote: have you learned anything about using the material for either magnesium wallboard or dead burned magnesium oxide or other commercial applications, or are you just looking to sell the MgO or metal itself?

JL: We will start with MgO but are now looking at upgrading some of the MgO to Mg Metal and will have an update on this shortly.

TCI: Something different. As we discussed in the past, is a Venture uplisting still out of the question? Do you have other uplisting initiatives planned in the near future?

JL: Yes, we will not be interested in Venture uplisting as it would still limit our dealmaking capacities; we can't act quickly and aggressive that way. One of the rules is also that you need to have two years of cash in advance in order to fulfill eventual deal terms in that period, and I don't feel that TSX should determine this for me, I can perfectly allocate cash myself. There are plans to uplist to the TSX and/or NASDAQ when revenues take off and share price and volume follow hopefully. This will likely not be before somewhere next year. For now, MGX already uplisted to the OTCQB for the U.S. markets.

TCI: Something else, which is communication with investors. I recently noticed you put up a presentation again after a long hiatus, which is useful for investors as MGX is busy with so many different projects. However, you also came out with no less than 14 news releases in January 2018. The last time we discussed this you explained most is regulatory as most news is material, but news like completion of a site survey, commencing a drill program by a JV partner or a separate news release on the "acquisition of patents" six weeks after acquiring the company that owns these patents isn't material enough for a mandatory news release and certainly doesn't seem to add a lot of value to put it mildly. Other news like hard rock lithium drill results seem eligible for having larger batches with more results at one time. Why continuing with this high frequency?

JL: Most if this is regulatory, MGX just has a lot of projects going on, also our shareholders like it this way, and the company gets more media attention overall, as the likes of Bloomberg pick it up as well.

TCI: Could you provide us with some background information about the latest financings?

JL: Sure. We wanted to raise C$7.5M non-brokered, part FT (half warrant) and part NFT (warrant), but there was a lot of interest and we ended up with C$12.9M. Sprott bought C$2.5M which was great to see. EMD Financial was leading the efforts this time, and they did very well as they brought in several new institutions. The FT proceeds are used for exploration (hard rock lithium, silica), and the NFT proceeds are used for the water treatment plants and acquiring and developing lithium assets in Alberta, California and Chile.

TCI: We discussed geothermal power in California the last time. Back then you indicated you liked to stay away from California in general because of environmental/permitting risks. Things seem to be changing for MGX lately?

JL: Yes, we have a much better network in California at the moment by attracting retired U.S. Senator Polanco, and are looking into geothermal plants again for lithium production. We are looking to partner with a company that has an interest in running the plant for energy supply, and we simply treat the heated water, which has relatively high lithium grade.

TCI: The patents on the nano filtration method are still pending. Is there a timeline on this?

JL: This could take a year from now, in the meantime we do have a U.S. provisional patent, though, that protects us.

TCI: Purlucid doesn't report any financials, but could you provide us with an indication of revenues based on the oil sands contract?

JL: Revenues for them are estimated to be up to C$2M per annum, and this can start in August of this year.

TCI: Could you tell us about the status of the Paradox Basin drill plan MGX was designing with AMP (American Potash Corp) last time we talked?

JL: MGX is adjusting this plan with AMP. There is in fact a drill plan, the target has been defined but MGX wants to do the 3D seismic first.

TCI: In January 16, 2018, a remarkable partnership with Highbury Energy was announced in order to extract nickel, vanadium and cobalt from petroleum coke. How did you develop an interest into this business?

JL: MGX Minerals was looking into this for a long time, as petroleum coke is relatively high grade regarding these metals and is considered waste, being a by-product of oil refining. Vast stockpiles of petcoke exist, to the tune of 106 Mt in Alberta alone. We wanted to get into the hydrogen business, and look into other battery metals as we saw potential here. We are after creating innovative processes and technology to shape the new energy economy.

TCI: As I tracked rare earths over the years, I noticed an August 29, 2017, news release about a REE project. Why did you acquire a REE project from your VP Exploration in a time that REEs can't be mined economically outside China?

JL: We believe the tide is turning on North American REE production. Strategically the U.S. cannot depend on China for REEs and with protectionist winds blowing it is time to look at completing exploration on this property. We want to drill it in order to get it to a resource, we applied for a drilling permit and expect to be able to drill shortly.

TCI: I looked at the 20% Case Lake JV regarding a hard rock lithium project. What is the objective here for MGX Minerals, do you have an exit in mind?

JL: Case Lake is an investment. We hold this 20% working interest in order to monetize it at a buyout. A 3,000m drill program is progressing, and we and Power Metals aim for an Inferred resource estimate being announced in three months from now.

TCI: Can you tell me the total acquisition price of ZincNyx Energy Solutions, a zinc air battery developer, and why Teck sold it?

JL: The total acquisition price was about C$4M, and to date C$15m has been invested in ZincNyx. Teck divested it to us as it wasn't a core business.

ZincNyx 5kW prototype

TCI: When I look at the containerized zinc air battery prototype, it looks like quite a massive installation for a 5kW continuous power battery. Might the planned 20kW battery be even bigger? When I compare this to Tesla Motors Inc. (TSLA:NASDAQ) Powerwall with the same 5kW output and storage of 13.5kWh, it is much smaller (115x75.5x15.5cm @125kg) and more convenient, and can be scaled up by just adding up to 10 Powerwalls. Pricing of a Powerwall isn't cheap but relatively low at $6,200. For the record I am not a big fan of Tesla but it is an interesting comparison. Do you have any idea of pricing, size and applications for the zinc air battery?

JL: There is a key difference between the Tesla Powerwall versus our ZincNyx Fuel Cell Battery that you didn't address. Our storage capacity is much larger, and in order to increase storage you just increase the size of the fuel tank and add more fuel (zinc in this case). To increase storage of a Tesla battery you have to add both output and storage capacity. This decoupling of output power and storage is key and makes the ZincNyx system much cheaper in terms of storage capacity. So, the real question is how much energy can you store, not just what is the rated output capacity. In terms of size, the system will be about the same size from 5kW to 20kW, as everything is shrinking in size in the production design phase at the moment with the exception of the fuel tank itself.

A standard 5kW system will have 40kWh storage; the new 20kW system will have 160kWh storage. The target price, like others in this space, has been $250/kWh for an eight-hour backup system. This would result in $10k for the 5kW system and $40k for the 20kW system. Depending on the application and configuration, the price can be significantly higher or lower. The fuel cells, needed for output, are the expensive part of the battery. With economies of scale, prices would go down.

TCI: The separation of power and storage is interesting, as it provides options as you say. I noticed you recently kicked off development of the new 20kW battery at ZincNyx Energy Solutions. Isn't there an extensive certification procedure involved for safety reasons, which could take a long time? You talked about mass production for mid-2019; do you have contracts/manufacturing means in place for this?

JL: Yes, we already have partners for manufacturing and this has been underway for a number of years. Certification is primarily the same as any standard appliance and there is no specialized testing required that we are aware of.

TCI: I feel we have discussed most topics now, so it is time to come to a conclusion. Could you tell me about the most important catalysts coming up? If you have anything else to say for our readers, feel free to share of course.

JL: There is a tremendous amount going on and every month there will be significant catalysts in lithium, petrolithium, magnesium, mineral extraction processes for battery metals, and energy storage but with a single energy or energy materials theme with all divisions marching towards the same goal, which is revenue or monetization of assets.

TCI: Thank you for your time, Jared. This update hopefully provided new insights, and might enlighten the shift from numerous clean energy projects to actual revenues and NPVs. I am looking forward to the moment I can actually value the most important assets of MGX, get forecasts on revenues/cash flows, and hopefully see MGX becoming a major player in respective cleantech technologies. 2018 will be an important year for MGX Minerals, as it will be the year of proof.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu, and follow me on Seekingalpha.com, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Disclaimer:

The author is not a registered investment advisor, and MGX Minerals is a sponsoring company. All facts are to be checked by the reader. For more information go to https://www.mgxminerals.com/and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Want to read more Energy Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles with industry analysts and commentators, visit our Streetwise Articles page.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Images provided by The Critical Investor