1. Introduction

Last year has been a quiet year with the COVID-19 pandemic restricting most exploration activities in Argentina, but the situation has changed since November 2020, and Blue Sky Uranium Corp. (BSK:TSX.V; BKUCF:OTC) is back in business again, ready to advance its flagship Amarillo Grande uranium project. The company received a tailwind from positive sentiment for uranium companies in general, which has been fueled by several reasons. The most important one has been the U.S. Senate approving a bill which requires the U.S. holding a domestic reserve of uranium; another one has been the shutting down of operating mines like Cigar Lake, and reducing further development and production of mines in Kazakhstan. This and other causes resulted in a higher spot price for U3O8 in 2020, as is shown on this chart from the Cameco (CCO.TO) website:

This in turn lifted uranium junior stocks considerably after the March COVID-19 market crash, but as can be seen in the following 1 year comparative chart showing the five largest uranium mining stocks with a North American listing and Blue Sky Uranium itself, the U.S. uranium reserve bill ignited a real fire in December:

Multiple uranium company chart 2020 (Source: tmxmoney.com)

As the owner of a low cost uranium project in Argentina, Blue Sky Uranium also saw a 46% increase in share price over 2020, and received lots of interest from investors. Management didn't hesitate too long, announced a private placement of C$3.51 million @ C$0.13 and a full 3 year (C$0.25 exercise) warrant on December 29, 2020, and closed it heavily oversubscribed at January 26, 2021. A full treasury allows the company to advance its district scale Amarillo Grande uranium-vanadium project in the mining friendly Rio Negro Province in Argentina, as the company plans on expanding the existing NI43-101 compliant resource as much as possible, and is working on a Preliminary Feasibility Study (PFS). I expect a larger project to have improved economics, which are already pretty solid for a uranium project, as production costs are in the lowest quartile of the industry. What this could mean for investors will be discussed in this article.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. Company

Blue Sky Uranium is an exploration and development company, focusing its uranium and vanadium exploration efforts on southern Argentina, with 100% control of more than 300,000 hectares of mining tenures. The company is a member of the Grosso Group, lead by Joe Grosso, and is a resource management group that has pioneered exploration in Argentina since 1993.

The company's Amarillo Grande Uranium-Vanadium Project in the Rio Negro province is a district-scale uranium discovery and includes the flagship Ivana project, containing the country's largest NI 43-101 resource estimate for uranium, with a significant vanadium credit.

Blue Sky Uranium currently has, after closing the recent financing, 162.11 million shares outstanding (fully diluted 224.977 million), 46.7 million warrants (the majority is due @C$0.250.30 in 2022 and 2024),and several option series to the tune of 16.17 million options (C$0.250.30, expiring in 2023 and 2026) in total, which gives it a market capitalization of C$28.4 million based on a January 29, 2021, share price of C$0.175. Addition: on January 29, 2021, the company issued 12 million options with an expiry date of January 27, 2026, and an expiry price of C$0.25. As an explanation for the rather generous amount, CEO Nikolaos Cacos had this to say: "Stock options are an integral method of incentivizing a teamespecially one as dedicated and talented as Blue Sky's. The last time we granted options was over three years ago. As we embark on a new key phase for the company to expand our current resources and, potentially, add considerable new value, the Board felt it was the right time to ensure that those carrying out all this work are incentivized and can share in the success of the company's growth."

As we have seen recently, the company has no trouble raising cash, and this kind of money goes a long way for exploration (drilling) at its Amarillo Grande project, as all mineralization is near surface, at a maximum depth of just 30 meters. The share price keeps hovering at relatively low levels, but picked up somewhat as mentioned due to the U.S. reserve bill:

Share price; 1 year time frame (Source: tmxmoney.com)

This low pricing is predominantly related to the current low uranium prices for spot and contract, rendering almost all uranium projects worldwide uneconomic as mentioned. The uranium market itself is a very untransparent and therefore complex market to understand and surely forecast, but I will try to make things a bit more insightful in the next paragraph.

The management team of Blue Sky Uranium is also the core of the Grosso Group team, and is led by President and CEO Nikolaos Cacos, who has been with the Grosso Group since inception in 1993, and a director of Blue Sky Uranium since 2005, and a director of Golden Arrow Resources since 2004 and president and CEO of Argentina Lithium since 2013. All three companies are members of the Grosso Group, and operate in Argentina. CFO Darren Urquhart isn't that long with the group but also closely involved like Cacos as he is CFO of all three companies. With all three companies there is a specific metal specialist geologist on board, and with Blue Sky it is Guillermo Pensado, the VP of Exploration and Development, who has over two decades of experience in exploration and economic project assessment in the Americas, with most of it focused on uranium.

When we are talking about the Grosso Group, there is no way we can go around the founder and chairman, Joseph (Joe) Grosso. He became one of the early pioneers of the mining sector in Argentina in 1993 when mining was opened to foreign investment, and was named Argentina's 'Mining Man of the Year' in 2005. His knowledge of Argentina was instrumental in attracting a premier team, which led to the acquisition of key properties in Golden Arrow Resources' portfolio, of which the development of Chinchillas eventually resulted in a JV with SSR Mining. He has successfully formed strategic alliances and negotiated with mining industry majors such as Barrick, Teck, Newmont, Viceroy (now Yamana Gold) and Vale, and government officials at all levels. At the moment he is the chairman of Blue Sky Uranium, a director of Argentina Lithium, and executive chairman, CEO and president of Golden Arrow Resources, which is the flagship company of the Grosso Group. To me, Joe Grosso is instrumental and successful in managing any jurisdictional risk in Argentina, and very important for Blue Sky Uranium in this role.

Another important person is director David Terry, PhD Geo, who is an extremely knowledgeable geologist, has been with the Grosso Group for a long time, and currently is a CEO of Genesis Metals, and director of Golden Arrow Resources, Great Bear Resources and Aftermath Silver.

So far for management, let's have a look at the commodity in focus, which is of course uranium.

3. Uranium

Uranium (chemical element U, better known as U3O8) is the fuel for nuclear power plants. Many industrialized nations are heavily dependent on nuclear power generation, with nuclear electricity representing a major component in such countries as the United States (21%), Hungary (36%), Sweden (46%), and particularly France (78%). Japan used to be one of the biggest nuclear electricity producers (34%), but since the Fukushima disaster in 2011 all nuclear reactors have been shut down. Since Q3, 2014, Japan is slowly restarting reactors again.

As renewable energy (wind, water, solar) is becoming increasingly important, but it's main issues are its lack of continuity and directly connected to this a power grid that can absorb the shifts in energy levels, society needs sufficient base load power, and coal and nuclear can provide this certainty, and therefore will not go away anytime soon, especially nuclear since coal has been developing an increasingly negative environmental image.

Worldwide, 440 reactors supply about 10% of the world's energy requirements. In addition to this, 53 nuclear reactors are in various stages of construction worldwide, with Asia leading the pack, with China constructing 11 and India constructing 7 of these new reactors. There are also a number of reactors being phased out, so the nuclear utility fleet is expected to see a small annual increase.

These utilities buy uranium from producers, via long term contracts. World uranium production used to be dominated by Kazakhstan, Canada and Australia which, together, produced about 74% of annual mine supply in 2019. These countries are followed by Niger, Russia and Namibia. These leading producers combined account for approximately 95% of worldwide mine production. An important development in this regard are the production cuts by Cameco and Kazatomprom as a reaction on ongoing low uranium oxide prices. In 2019, world production of uranium came in at 142.3M lb of uranium, and figures of 2020 are not in yet, but are expected to be 129M lb according to consulting firm UxC. This actually seems a high forecast to me but we will see. The four largest producers for capacity are Kazatomprom, Cameco, Orano (former Areva) and ARMZ-Uranium One.

Cameco even shut down its last remaining operation Cigar Lake in 2020, for the second time that year due to COVID-19 measures, and ceased production completely. As a consequence, Cameco has been buying at the spot market since 2019 to fulfill its contract obligations. This led me to believe that the current spot prices, which are low compared to costs of production, are actually artificially kept at higher levels, because of producers like Cameco but also Kazatomprom buying at the spot market. They are not the only ones doing this, as for example traders, banks and hedge funds are buying uranium oxides left and right in order to speculate on future price increases.

Other operations around the world also saw COVID-19 induced production cuts, although marginally. Mines that are forecasted to halt production soon are Ranger in Australia and Arlit in Niger, and this is expected to have a meaningful impact on spot pricing.

Although current production is only 7580% of current demand and has been lowering for several years now, and there has been no demand destruction, spot and contract pricing remains at low levels. In general, US$60/lb U3O8 is believed to be the minimum threshold to bring most idled operations back online again, or start up new mines, but the current spot price lags at US$30.20/lb, and the contract price at US$35/lb. This remarkable situation can only exist because utilities, the primary buyers of uranium oxide, have large multi-year stockpiles, as they cannot afford the risk of shutting reactors down due to lack of fuel. In addition to this, closed Japanese utilities keep selling on the spot market. On an important sidenote, fuel accounts only for 23% of the operating costs of a utility, so in my view they don't care less if prices hover at US$20, US$30, US$60 or US$100/lb, and are certainly not waiting until spot prices are rising as other market commentators have been implying.

The million dollar question was, is and always will be in the uranium sector: when the utilities will start coming back to the contract market in order to arrange new long term supplies, usually for 5 to 10 years? When this happens, it is anticipated that demand will outstrip supply in such a way that spot and contract prices will have to rise substantially, as current halted mines can't be switched on quickly enough.

These restarts take time, to the tune of 0.752 years, and when Japanese selling on the spot market has dried up and utilities start buying, there is no time. Although I believe there could be a spike in pricing again, it is also my opinion that we will not see the extremes of 2007, with spot prices going to US$136/lb and contract prices to US$95/lb:

As Kazatomprom seems to have control over supply these days, as it can increase production relatively quick and easy, I do believe that it will find a way to increase production at such pace that an eventual peak in spot prices will not supersede US$60-70/lb U3O8, and contract prices will remain at US$50/lb U3O8 or lower. In this way it prevents most undeveloped projects from being financed, as the very best projects need a long term US$50/lb price, and the average project US$6065/lb, so Kazatomprom would remain in control.

For now the most important development on the short term will be the confirmation of the Biden presidency of the U.S. uranium reserve bill, signed by his predecessor Trump. Biden has stated in the past that he is a supporter of implementing SMR (small) nuclear reactors. Notwithstanding this, the first utility signing a long term supply contract will be the real game changer for the mining industry.

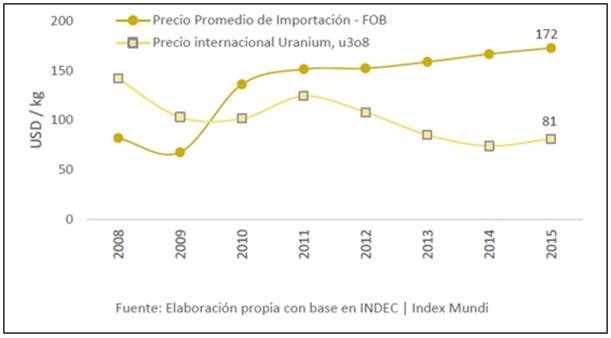

Let's have a quick look at the situation in the jurisdiction where Blue Sky Uranium is operating. Argentina has no current uranium production on home soil, and requires 100% importation of its uranium supply. The country has three nuclear reactors generating about 5% of its electricity; its current annual consumption is approximately 300 tonnes U3O8 (or 660,000 lb U3O8). As shown below in an outdated but still relevant chart sourced from the Mining and Energy Industry of Argentina, the price paid for uranium was much higher than the international market price for uranium:

It doesn't look like this situation will be adjusted anytime soon in Argentina and provides an excellent future environment for Blue Sky Uranium and the Grosso Group to negotiate with the government on long term off-take contracts for its Amarillo Grande project. After focusing on the macro environment for uranium, it is time to look at the project itself.

4. Amarillo Grande Project

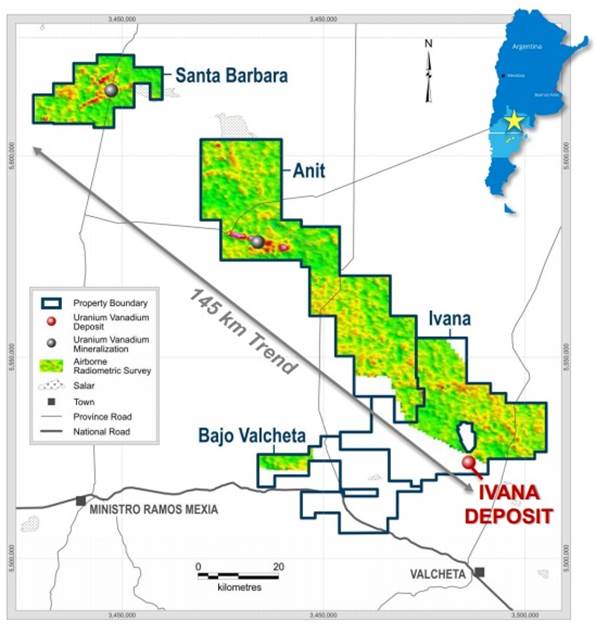

The Amarillo Grande Project, located in the Rio Negro Province in Argentina, covers over 300,000 hectares of mineral exploration rights. The province has a 38 out of 76 ranking on the latest Fraser Institute Survey of Mining Companies. Within this, the Ivana group of properties containing the flagship Ivana project covers over 118,000 hectares north of Valcheta City in Rio Negro Province. It is the southernmost property along the 145 kilometer NW-SE trend, of which only 7,000 hectares have seen recent exploration, that contains not only the Ivana deposit but also a series of airborne radiometric anomalies that represent future exploration targets.

The remaining 111,000 hectares also represent a lot of potential for multiple blind deposits, related or not to superficial anomalies according to management. The project has year-round access through a well-maintained gravel road network, in an area of very low population density. The project is in a semi-arid topographical depression, close to 100 meters below the elevation of Valcheta City (25km south of the Ivana deposit and the location of the regional office of Blue Sky Uranium), with low rainfall, and within a closed hydrologic system. Therefore, any mining and processing activity developed in the area would likely have a low potential risk to local fresh water aquifers.

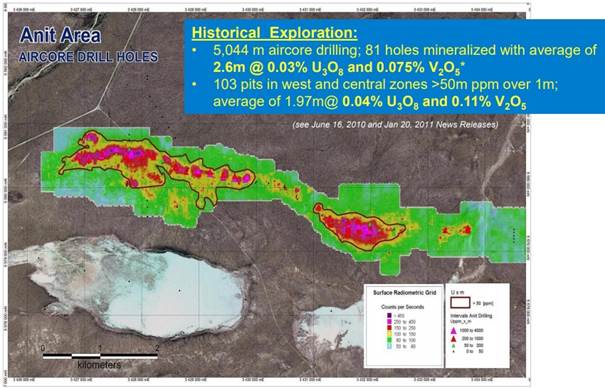

Blue Sky Uranium has been exploring the Amarillo Grande Project since 2006, and came up with interesting results for the initial Anit and Santa Barbara targets. Lots of historical RC drilling returned widespread uranium and vanadium mineralization:

Management never completed a resource estimate on Anit, as the uranium market went into a downward cycle, following the 2011 Fukushima incident, and focused on Ivana when things normalized, but based on these historical exploration results and size, I would like to estimate a mineralized envelope of 4,000 x 500 x 2.3m x 2.1t/m3 = 9.66Mt, which would result in 6.3M lb U3O8 and 15,78M lb V2O5.

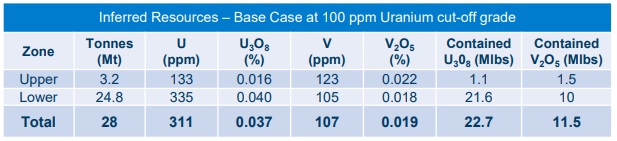

The later discovered Ivana deposit is the most economic project so far and therefore probably the first to be developed, but management hasn't forgotten about the other two projects, or the various radiometric anomalies along the 145km long potential exploration trend. The Ivana deposit is a surficial deposit with a NI43-101 compliant Inferred resource of 22.7M lb U3O8 and 11.5M lb V2O5:

According to management, this new district may be hiding multiple blind deposits, and its potential may be not only at surface but also in depth, as suggested by Areva in its exploration program. The Blue Sky exploration team, armed with the experience of the Ivana deposit discovery and the development of an exploration model to be applied all over the district, is now focused in the re-assessment of the Anit and Santa Barbara surficial mineralizations, as well as the several radiometric anomalies in between. Management thinks that those areas may represent the superficial expression of multiple blind, deeper and higher grade roll front deposits representing an estimated potential for about 100M lb U3O8 along the entire district. I asked them specifically how they got to this concept. This is their explanation and in my view the key to the story:

"The surficial mineralization is the indicator itself because roll front deposits, or the uranium comprised in those deposits, can be remobilized by oxidized ground waters and precipitated as surficial mineralization near surface. This is the model observed at the Ivana deposit. Therefore, the several radiometric anomalies along the 145km long district, including Santa Barbara and Anit, may be indicating deeper blind deposits."

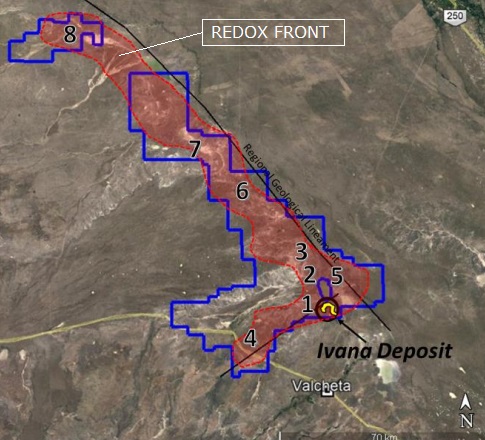

The Ivana deposit contains layers of poorly consolidated sediments that are calcareous, but the strength of the calcite cement is far from being considered calcrete. The absence of these calcrete layers improves metallurgical recovery a great deal. The primary uranium mineralization at Ivana also has considerable similarities to sandstone-hosted uranium deposits in other locations, particularly basal-channel sandstone-hosted uranium deposits, and appears to be related to a redox boundary of possible regional extent.

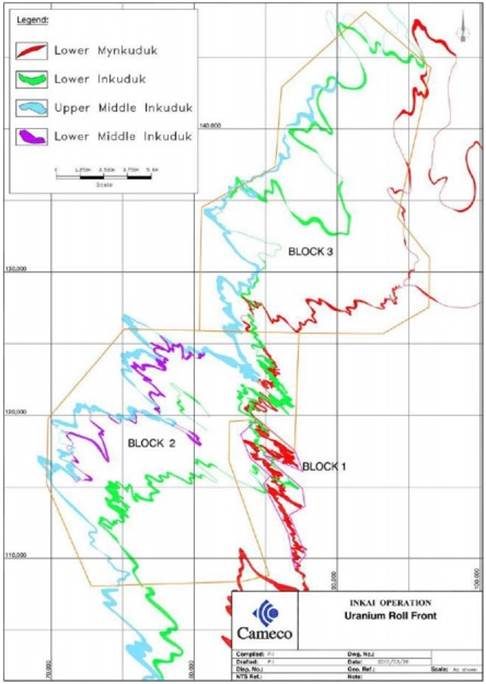

Uranium deposits of this type formed along regional redox boundaries can reach large sizes, as at Inkai, Kazakhstan, where the proven and probable reserves are about 270 million pounds of U3O8 at a grade of 0.03% U3O8, and in situ recovery (ISR) production at these deposits (JV of Cameco and Kazatomprom) currently dominates global supply.

Of course, this doesn't directly imply that Ivana could get very large as well, but as Blue Sky Uranium has traced uranium on a district scale trend here, this could indicate significant potential in that direction. The company has staked 145km of claims now, covering almost a complete anticipated redox boundary front:

The Ivana uranium-vanadium deposit is currently considered a hybrid, in part a surficial deposit, and in part a sandstone-hosted deposit. It has the following features:

- Hosted by loosely consolidated sediments from surface to just 24 meters depth; mining via open-pit methods

- Oxidized uranium-vanadium mineralization amenable to upgrading by simple wet scrubbing and screening and alkaline leach processing

- The Ivana deposit remains open for expansion and additional near deposit (or brownfield) exploration resource potential exists in the Ivana area

The company completed a preliminary economic assessment (PEA) on the Ivana deposit at February 27, 2019. The report described an open pit operation with a 13 year life of mine (LOM), a 6,400 tonne per day throughput and a strip ratio of 1.1:1.

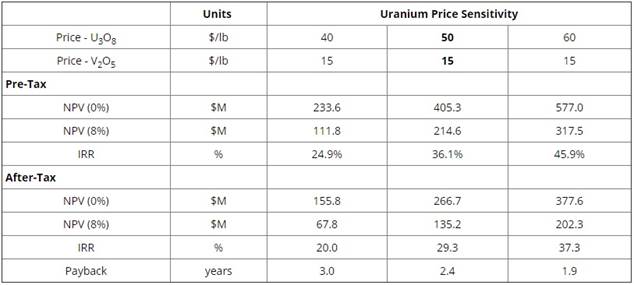

Overall recovery of uranium oxide is 84.6%, and of vanadium pentoxide 52.5%, which is solid. The annual production is 1.35M lb U3O8 on average, which would make Ivana a relatively small uranium project, but as mentioned management sees potential to increase the total amount of pounds to about 100M lb. The PEA shows decent economics for a uranium project: at US$50/lb U3O8 and US$15/lb V2O5 the post-tax NPV8 is US135.2M, IRR is 29.3% and capex is US$128.05M. The sensitivity looks like this:

So despite the low grade mineralization, the Ivana project manages to become economic at US$50/lb U3O8, ranking it in the lowest quartile of projects under development, whereas many peer projects or mines in care and maintenance need US$6065/lb U3O8 nowadays. The McArthur Mine of Cameco might even need higher uranium prices, as it needs a pretty expensive upgrade before production can resume. Beneficiary factors for Ivana are of course the very near surface mineralization and low strip ratio, and the very soft host rock.

Because of the vanadium by-product of about 10% of revenues, the all-in sustaining costs are pretty low, at US$18.27/lb U3O8. This means as long as the Ivana project gets financed and put into production, it could endure Argentinian uranium oxide contract pricing as low as US$20/lb.

The base case price for vanadium was set at US$15/lb, which looked realistic when the PEA was released, but unfortunately is no longer applicable as it trades at US$7/lb at the moment, meaning revenues would drop 5%. Running a quick back of the envelope estimate, I expect after-tax NPV8 to drop to about US$120 million, and IRR to 27%, which are still very decent numbers and still imply a lowest quartile producer. So the vanadium isn't really that important to the project. Vanadium could be an interesting contribution in the future, as vanadium pricing showed some extreme spiking over the longer term:

As can be seen, US$15/lb is relatively high compared to long trading price levels, and since 20052006 it seems to revert back to US$56/lb after spikes. Notwithstanding vanadium pricing, if Blue Sky Uranium does manage to delineate 100M lb U3O8, it isn't unrealistic in that case to double or even triple production capacity and double LOM. In this case some economies of scale could kick in, and despite expected lower average grade and increased capex, the post-tax NPV8 should be able to come in at least around US$300350 million, with the IRR roughly estimated at 2527% as well, maybe higher depending on the amount of higher grade ore the company could delineate in the future.

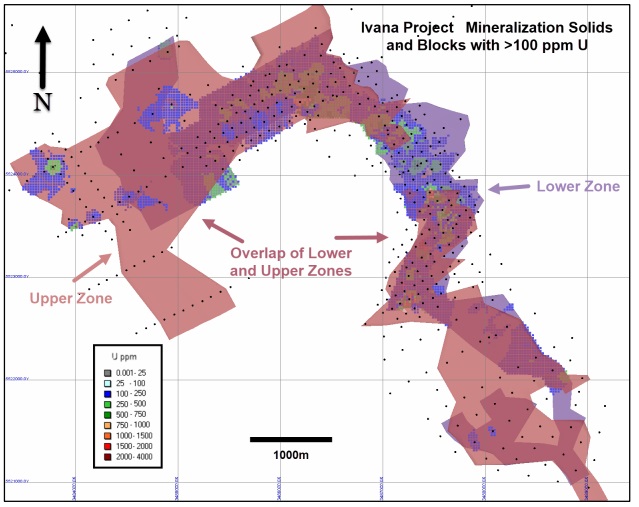

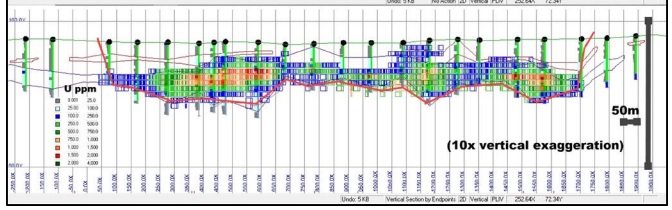

The company is proceeding with the expansion of the current resource and setting up work programs for the upcoming PreFeasibility Study (PFS), and for this it is not allowed to include Inferred resources, so these need to be converted. The current resource looks like this in the following schematic map projecting drill holes as well:

The following section shows a slice exaggerated in height, as it is spread out and relatively thin:

The current drill spacing of 100 x 200m appears to be adequate to update Inferred into Indicated resources but this is up to the geologists; however, more extensive bulk density testing is needed before the resource can be moved to the Indicated category.

Blue Sky Uranium also has numerous projects in the Chubut province. Situated directly south of Rio Negro, Chubut hosts several uranium deposits, however, none is currently in production and the provincial government has enacted restrictions against open-pit mining. The company's projects in this area, Sierra Colonia, Tierras Coloradas, Regalo and Cerro Parva, comprising more than 150,000 hectares of 100% controlled mining properties, are shelved now because of this.

For now, Blue Sky Uranium is planning RC drilling to expand the Ivana Central and North zones. For Ivana East and Cateo Cuatro, targets are being advanced toward drill testing. Management also plans to look for potential for in-situ recovery (ISR) zones at a larger depth, but no deeper than 150 meters, in analogy with the Kazakh deposits. Furthermore, the company will be looking into restarting drilling at Anit and Santa Barbara.

5. Conclusion

The recently signed U.S. uranium reserve bill has injected the uranium juniors with fresh energy. As more and more operating uranium mines are put on care and maintenance, and demand keeps increasing steadily, many experts feel the point of utilities finally starting to arrange long term contracts is coming near. The markets are sharing this positivism, and Blue Sky Uranium capitalized on it by closing an impressive C$5.46M financing, which is enough to take the company through a busy year of advancing Ivana toward resource expansion and starting preparation for a PFS.

The company has a few robust advantages over many other uranium developers: in Argentina uranium oxide is imported at a much higher price than used at the international markets; its Ivana PEA already indicates a profitable project at US$50/lb U3O8, which places Blue Sky Uranium in the lowest quartile of developers and producers; and lastly it has substantial growth potential as management believes it could expand the existing resource up to four times. If it will succeed remains to be seen, but I like its chances.

If you are interested to hear more from management, they will be presenting a webinar on February 2, 2021, at 4:05PM EST together with Amvest Capital, and if you want to participate you can sign up through this link:

https://attendee.gotowebinar.com/register/5598786188867828237?source=co

If for some reason signing up doesn't work or if you have other questions, feel free to contact management per the contact details on blueskyuranium.com.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on www.criticalinvestor.eu in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

[NLINSERT]Disclaimer: The author is not a registered investment advisor, and has a long position in this stock. Blue Sky Uranium is a sponsoring company. All facts are to be checked by the reader. For more information go to www.blueskyuranium.com and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver and Blue Sky Uranium, companies mentioned in this article.

Charts and graphics provided by the author.