As I write this missive, we have just entered into the six most dangerous months of the year after experiencing the ninth best month for performance in five decades. The S&P 500 closed up 9.75% in the month of April, with the NASDAQ registering its best performance since April 2020, up 15.29%.

What is surprising is that there have been no surprise stimulus efforts made by either the Fed or the Treasury to substantiate these types of performances. Furthermore, with oil pressing up and through $100/bbl. to close out the month, interest rates have moved higher in anticipation of a resurgence of inflationary pressures, with the 10-year 4.40% and the 30-year knocking on the 5% door, and the Strait of Hormuz remains firmly impassable.

You will recall that the original mission in Iran for the American armed forces was to accomplish three things:

- Recover nuclear materials used in making weapons

- Regime change

- Eliminate Iranian control over the Strait of Hormuz

To date, none of these objectives have been met — repeat, NONE — and yet the President this afternoon sent a letter to Congress declaring that "Hostilities have ended" with regard to the war. One has to wonder how permanent this "cessation of hostilities" will remain if those tankers two months from now are still unable to secure safe passage through the Strait.

This morning I posted chart of the QQQ:US which clearly illustrates how deeply overbought the tech stocks have become, and since the QQQ:US has a unique mix of mainly tech stocks in its portfolio, the resurgence of the Mag Seven has been its driver.

Top 10 QQQ Holdings:

As of May 2026, the top 10 securities make up approximately 46.7% of the fund's total assets:

- Nvidia Corp. (NVDA:NASDAQ): ~9.26%

- Apple Inc. (AAPL:NASDAQ): ~7.10%

- Microsoft Corp. (MSFT:NASDAQ): ~5.70%

- Amazon.com Inc. (AMZN:NASDAQ): ~4.98%

- Meta Platforms Inc. (META:NASDAQ): ~3.54%

- Alphabet Inc. Class A (GOOGL:NASDAQ): ~3.64%

- Alphabet Inc. Class C (GOOG:NASDAQ): ~3.38%

- Broadcom Inc. (AVGO:NASDAQ): ~3.39%

- Tesla Inc. (TSLA:NASDAQ): ~3.35%

- Walmart Inc. (WMT:NYSE): ~3.08%

In fact, of the top ten securities held by this ETF, only Walmart Inc. (WMT) is not a member of the technology sector.

Also breaking records in the month of April was the Philadelphia Semiconductor Index ($SOX:US), which posted eighteen consecutive record highs in the month. Despite a couple of down days during the last week of the month, it registered a near-record close for the month on Thursday and earlier today hit yet another record high at 10,595.07 before easing off.

Every momentum indicator on the board is flashing "overbought" while the folks over at CNBC are trotting out Tom Lee every ten minutes so he can restate his forecast for the semis over and over again, which, to no one's surprise, is "serially bullish".

The Shiller CAPE ("cyclically-adjusted price-earnings") ratio is also screaming a warning. As of early May 2026, the Shiller CAPE ratio for the S&P 500 is hovering around 40.24.

This level is historically extreme, marking only the second time in the 155-year history of the metric — dating back to 1871 — that valuations have exceeded the 40-point threshold for a sustained period.

Current Valuation Context

- Historical Average: The long-term mean is approximately 17.3. The current reading represents a 135% premium over this historical norm.

- Modern Context: Since 1976, the average has been higher at roughly 22.7, but the current ratio remains significantly elevated even by modern standards.

- Year-over-Year Change: The ratio is up approximately 22.6% from the same time last year, when it sat at 32.62.

So, with momentum off the charts in terms of being "stretched" and valuation now approaching levels not seen since the DotCom bubble, if it looks like a bubble and it acts like a bubble, maybe — just maybe — it is a bubble.

A few ETF's are lurking about that can provide investors with decently correlated proxies for lower prices. The one I particularly like is the Direxion Daily Semiconductor Bear 3X (ARCA) ETF (SOXS:US), which one year ago traded 32.5 times higher than today's price at its 52-week high of $423 as compared with the current bid price of $12.93. To put April's moonshot into perspective, one month ago today, it traded at $38.49, nearly triple the current price.

Now, as a disclaimer, please be forewarned that these leveraged ETFs have a sneaky habit of eroding in value with the passage of time, so this ETF by no means represents a vehicle for the "BUY-and-HOLD" crowd. It is for traders and should be traded when and if a suitable profit presents itself (which could be never).

Materials

CNBC took great glee in announcing a few minutes ago that the only sector not advancing this week was the Materials sector. The Materials sector (also known as Basic Materials) includes companies "that discover, develop, and process raw materials used as foundational inputs for other industries".

That includes the miners which are suffering from a severe hangover brought on by the month-long party they all had in January, led by the premature celebrations of the silver bulls who are still delivering headlines like "The Comex Silver Crisis is Real" and "$309 Silver Right Now: The Forecast that Really Makes Sense " which are mere afterthoughts and in no way come close to Michael Oliver's now infamous "$500 Silver by Summer!" which was retweeted out fifty million times in the days and weeks after silver put in its classic top on January 29.

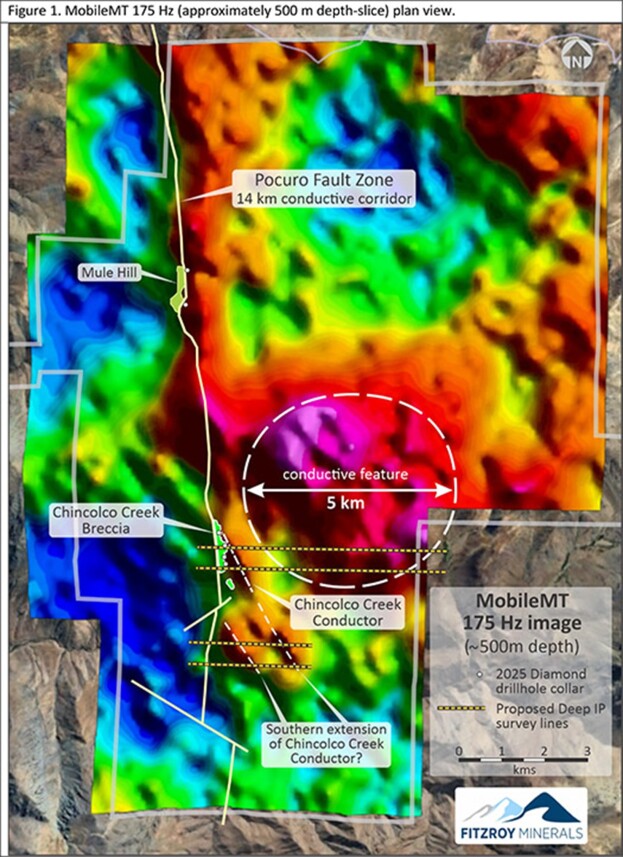

I bought the March 20 lows in the GDX:US and GDXJ:US and took profits on the leveraged parts of both trades at the peak of the bounce around mid-April, and now whatever I own is paid for by those trading profits. In the interest of full disclosure, I did not expect the miners to roll over and head down to what now appears to be a re-test of those March lows. In fact, if I were forced to hazard a guess, I would pick mid-late August as a possible turning point for the metals as well as the entire "Materials" group. There will be trades that show up in the miners from time to time, but a series of lower highs and lower lows is never a good space in which to reside. What I don't want to see is the March 20 lows fail to hold because if we break that level, the entire precious metals complex will be in jeopardy. Since the miners have always led the physical metals in terms of trend change, I would shudder violently if those March lows are taken out. It isn't just that the miners will all be headed lower, but it will cast a dark shadow on the January highs in that traditional technical analysis would have to shed a revisionist light on silver's bubble-like ascent to $121 per ounce and gold's awesome march to $5,626. The PM-bashers led by the crypto-gang are already pointing to the January 29th reversal as the beginning of the bear market in gold and silver, but from where I am perched, gold shows zero evidence of a bear market arrival. Silver's reversal of 48% from the January highs to its nadir a week later, around $62, is a different story and topic of fierce debate, as it is tough to view the last three months as anything but the early stages of a bear market. The sideways "chop" we have seen in both gold and silver has provided little in the way of clues as to the next major move, which is, by the way, in contrast to the action in copper, which has been grinding higher since it put in its low around $5.23 back in early February. I see no evidence of any disruption in the copper bull whatsoever, and continue to accumulate copper juniors with advanced exploration projects and established resources, with particular and honorable mention going to Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB).

The company released results of their helicopter-borne MobileMT airborne electromagnetic and magnetic survey ("MobileMT") completed by Expert Geophysics Services Inc. ("EGS") on Wednesday, with the highlight being that 5 km. wide anomaly shown in the graphic posted above.

I was explaining to subscribers the significance of the upcoming deep IP survey to be carried out this month, as it was explained to me by CEO Merlin Marr-Johnson, with the assumption being that this anomaly will carry "chargeability," which is a characteristic of sulphides associated with porphyry copper deposits. An IP survey will confirm "chargeability" and as I wrote in my email alert on Thursday, "I realize that this is a lot of information to absorb, especially for subscribers that are relatively new to the world of mineral exploration, but this IP survey will almost completely rule out other 'chargeable' materials, leaving the most likely material as "sulphides".

Given that Fitzroy has already identified copper-moly-gold sulphides on the fringes of the system, the odds are that any big chargeability anomaly will have Cu-Mo-Au in the sulphides mix. In short, Cu-Mo-Au-bearing sulphides associated with a porphyry are precisely what FTZ/FTZFF expect to find when they drill this target in the Fall. The IP survey will increase our odds of discovery which is why I am telling you. If this beast carries "chargeability", I will add aggressively to my position."

The results of the IP survey should be out by the end of the month or very early June, with the drill program commencing sometime in September, after the start of the Chilean springtime and the Andean snow has melted. In the interim, the stock is down some 39% from the January 28th high of CAD $.73 and represents an outstanding opportunity for the aggressive investor/speculator.

Canadian Markets

Canadian markets are shrugging off all kinds of negative economic data, but they have yet to eclipse the March peak, with the TSX Composite Index well off the record high recorded on March 2nd (the second day of PDAC). The TSX Venture Exchange, which houses the vast majority of junior resource issues in North America, is faring not-so-well as it is now 15.5% off the record high recorded on January 26th, three days before the blow-off top in gold and silver.

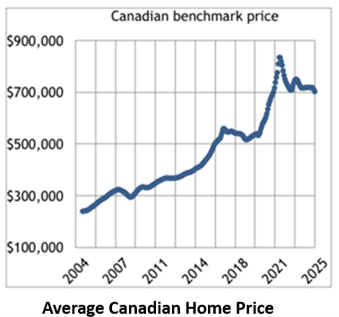

Canada is suffering from many things these days, not the least of which is the fact that most of the wealth in the country is now centered solely in residential real estate. The reason for this is that the baby-boom generation (of which I am a card-carrying member) has a vested interest in keeping the bubble inflated. Most of my wealthy male friends who have survived intact with the same wife of fifty or sixty years have been totally content to own the Canadian bank stocks and the house they bought in 1985 for $300k, followed by the cottage in Muskoka they bought for $250k in 1988, because that is the only equity they have in their entire 65-75 years on the planet. If the Government of Canada were to impose a hefty tax on second properties or on primary residences, the price of a normal house would drop by a hefty 50% overnight.

The realtors I speak with in the local area (which is NOT the Greater Toronto Area) are bleeding from the eye sockets because no one is buying OR selling.

The sellers are "forced sellers" because they bought at the top, banking on a "flip" and after three years of waiting for the "ten bidders above asking price" for their million-dollar "fixer-upper", they are now six months behind on their payments and their lender has finally been forced to foreclose. This phenomenon is only going to increase as time goes by, as the regulators are finally forced to lower the boom on the lenders and finally mark their loan portfolios to the real market rather than the expected market of the former bubble. Canadian residential housing is the true definition of the term "bubble".

Hong Kong residents looked at Vancouver in the 1960's and determined that it would be a better place to sow long-term roots than an island soon to revert to Mainland China so they moved their wealth and their families to Vancouver in droves and as long as they met the "Landed Immigrant" rules which included a net worth of in excess of $250,000, they came in with billions of Asian dollars, converted them to loonies and two-nies and inhaled every property in West and North Vancouver with reckless abandon. Even East Vancouver became the favorite point of RE speculation, such that houses such as the one shown here became tokens in the shell game of Vancouver property flipping.

The young family raised in Burnaby by parents of modest means was forced to vacate the basement of the family home and relocate to Kelowna, Surrey, or Penticton, not to find a job but simply to afford a roof over the heads of their young family members. The issue of "suitable employment" becomes a non-starter and defaults to a demand and dependence upon "government subsidy" in order to survive. This is exactly the fault of the generation that earned modest incomes for the majority of their lives, which gave their bank-owned government the God-given right to inflate the money supply in order to inflate the real estate market, only because their only real asset was the home in which they lived and/or the cottage to which they traveled in the summer. Today, those assets are egregiously over-valued, over-priced, and over-hyped, not only by the realtors trying to sell them, but by the banks whose loans are collateralized by the assets.

Now that the pin has touched the outer membrane of Canada's real estate "bubble", the banks are turning in panic to the government for a bailout because they realize that there is no bailout coming. The "boomers" no longer control the voting booth, and the kids know it.

Now that the pin has touched the outer membrane of Canada's real estate "bubble", the banks are turning in panic to the government for a bailout because they realize that there is no bailout coming. The "boomers" no longer control the voting booth, and the kids know it.

When the next election rolls around, housing "affordability" will be at the top of the "issues" agenda, and that means that either wages are going to be allowed to rise, or those with second and third houses as "investment properties" are going to be taxed into insolvency.

The main driver of the Canadian economy since the 1950's has been construction and real estate as the young and exceedingly sparse population of post-WWII was allowed to grow through mass immigration, much of it from members of the Commonwealth and of course, Hong Kong, whose ownership slipped from British rule in 1997. The banks were the primary beneficiaries of this wave of population growth, but it wasn't until the GFC in 2008 and the subsequent opening of the money-printing Bank of Canada spigot after the COVID pandemic that demand for housing exploded, taking the benchmark price through the proverbial roof.

While prices are cooling, the mortgage exposure to the Big Five Banks is substantial and that does not include Commercial Real Estate in the discussion. There was never a reason that a country as vast as Canada should have ever experienced a housing shortage but since the banks have had a stranglehold on Canadian politics from Day One, the growth of their mortgage books has been an enormous source of revenue and profits.

There are not very many young families that can afford the down payment to begin with, and if they are fortunate enough to have parents who can pony up the cash for the down payment, the young family is stuck with paying interest to the banks for the better part of their time on the planet.

If the banks had zero exposure to the underlying collateral (housing prices) you can wager your retirement savings plan that house prices would never have reached the dizzying heights of 2023.

The good news is that the global commodity cycle has turned, with demand for metals critical to the growth of electrification and the "AI" wave now being sought after. Canada is a veritable warehouse of critical metals, and while it has enjoyed a long and venerable history as a country of miners and oil drillers, we have not seen the kind of prospecting activity in decades that has been developing recently.

We need a shift in attitudes at the governmental level in order to protect and promote the commodity boom, but I dare not delve into politics as it is not exactly my chosen field of endeavor.

As for the Canadian currency, there has never been a commodity cycle that did not see the loonie advance against the U.S. greenback, which means investing in Canadian companies if you are a primary user of U.S. dollars should provide a firm tailwind. The S&P/TSX Composite Index (formerly the "TSX 300") has a 35.5% weighting in resource companies with roughly 18% Energy and 17.5% Materials (commodities).

As such, the upcoming commodity cycle is going to provide support for the index. As for the S&P/TSX Venture Composite (formerly the "TSX Venture Exchange"), it has a 66.2% weighting in resources, with Materials at 49% and Energy at 17.2%. Accordingly, if you are a metals bull, the TSXV is where you will get the biggest bang for your buck when the commodities cycle kicks into gear.

Demand for all metals associated with electrification and technology is growing into a global battlefield, with the Americans late to the party while China has been making inroads (as in "deals") throughout Africa and South America for the past two decades. Now that American leaders have woken up, they are moving with rapier-like speed to streamline the permitting process for new mineral projects so as to remove any and all shreds of dependence upon Chinese domination (i.e., "vulnerability"). The move to replace Venezuelan leadership was a clear statement to the Chinese that the Western Hemisphere is not going to become their playground when it comes to energy and raw materials.

My portfolio is centered around the theme that two metals will be front and center for the rest of this decade. Gold is the metal that prevents me from getting "debased" by the profligate explosion of the monetary base in most of the G7 nations, while copper is the metal that is in structural deficit while experiencing unfathomable increases in demand due to both electrification and technology ("AI"). Both of these metals dominate the junior explorers and developers that populate the S&P/TSX Venture Composite, and it is the juniors that make all of the new discoveries around the world, a phenomenon dating back to the 1980's. Since the leverage is in the juniors, a portfolio of well-researched junior explorers and developers is well-positioned for the wave of exponential growth that will occur before this next commodity cycle has run its course.

Lastly, the events of the past two months in the Middle East will be seen as a mere hiccup in this burgeoning commodity cycle, and I view weakness in gold and copper as one of the truly great investment opportunities of the last fifty years. It is time to look beyond the war; it is time to look at your list of investments.

It is time to move…

| Want to be the first to know about interesting Technology, Silver, Oil & Gas - Exploration & Production, Artificial Intelligence, Gold and Copper investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Apple Inc., Tesla Inc., Amazon, Alphabet Inc. Class C, and Fitzroy Minerals Inc.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Fitzroy Minerals Inc. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.