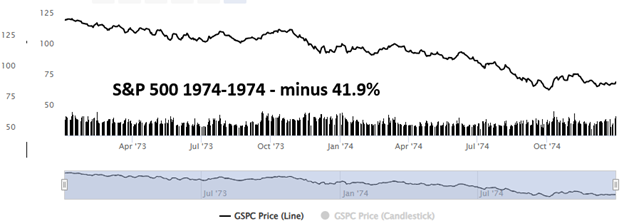

Back in the 1970's, as I was toiling diligently within the halls of Saint Louis University to complete my business degree, I witnessed long line-ups of frustrated drivers waiting diligently for the arrival of the tankers to re-fill the empty reservoirs at gas stations around the city. In fact, with then-President Richard Nixon battling to preserve his presidency, the S&P 500 was in slow but perpetual decline, dropping 41.9% in the same period.

When I first entered into the Canadian securities industry in the spring of 1977, veteran stock salesman at my firm would relay stories of the Great Bear Market of 1973-1974 when the vast majority of those living the good life in the Go-Go Sixties were forced to sell cottages in Muskoka and homes in Toronto's upscale Forest Hill neighbourhood after their clients (and their six-figure incomes) vacated the premises. In fact, as empty were the reservoirs at gas stations in 1974, equally empty were the bank accounts of customers the world over that stayed focused on the "Nifty Fifty" group of stocks (IBM, Coca-Cola, and MacDonald's), all of which crashed and burned along with the net worth statements of securities executives.

I have relayed before the story of a now-defunct brokerage firm, once considered a boutique on Bay Street, that had the most ostentatious of offices proudly situated at Bay and Bloor in 1972, rip out the offices and then state-of-the-art telephone systems only to replace them with a bank of pay phones so that the brokers (now cab drivers) could call what few clients that remained active while they ate their brown-bag lunches, cabs dutifully parked on the street below.

Kiddies with securities licenses today can be found flipping "AI" stocks or crypto ETF's, happy to use any utterance by a Fed official or an market-obsessed president vaguely tinged with "stimulus" as an excuse to "BUY BUY BUY!" all the while they trot out their business cards with the term "wealth manager" or "retirement specialist" or "portfolio manager". Not one of these kiddies has ever endured anything resembling the 1973-74 bear market that mauled investors with little of no respite for twenty one months — six-hundred and thirty days of financial agony as loss after loss ate away at savings, nest eggs, and once-mighty retirement accounts.

The look on the faces of salesmen (as opposed to "financial advisors") that endured that horrific period is a telling one as their eyes glaze over and they stare off into the distance while recounting tale after tale of heartbreak and ruin of someone they knew during the good times. While there are some that point to Watergate as the culprit that ushered in the bear, there was really only one perpetrator of the crime and that was a massive spike in the price of oil.

However, while the explosion in oil prices from $4.00 to $34.00 in the early 70's was the initial drivers for inflation, the Fed was behind the curve by about a country mile, failing to take notice of the escalating gold price which had been freed from its dollar peg by Nixon in 1971. As Americans struggled to keep their cars on the road without sacrificing their grocery budget or mortgage payment, there were a group of very savvy investors that were able to quickly make the transition from "blue-chip brokers" to "resource players" such that by the time I joined the industry in 1977, there salesmen driving the big new cars and buying all the power-of-sale cottages in Muskoka were wearing Stetsons and talking about "West Pembina" and "Dome Petroleums" while seated inconspicuously at the back of the brokerage bullpen. Adorned in tweed or leather blazers and wearing colourful ties or ascots, there were no pin-striped suits or Buster Brown shoes and nobody talked about bonds or blue-chip stocks. The action was in the junior oils and to a lesser degree in the gold miners (particularly the South Afrikaan gold miners) that were all rising as quickly as were the prices for oil and gold and the U.S. inflation rate.

Today in April 2026, CNBC is still locked in the daily drone of coverage for all of the companies that led investors during the bull market that actually ended in October of 2025. Sadly, as is the case with all bull markets that end, investors (and the financial news media) are still anchored in past glories and bygone victories. In fact, on Friday, I heard an analyst still talking about the "AI buildout" some five months after Nvidia Corp. (NVDA:NASDAQ)hit its all-time high above $212. Down 6.48% year-to-date and 16.40% from its ATH, the poster child for the last bull market is barking a different story as missiles fly in the Middle East.

If there is one lesson taught with cruel intent and debilitating discipline, it is that one should never stay too long at any party, particularly one that has the host walking around constantly telling you what a great time you (and everyone else) is/are having as you are weaving your way to the lavatory to relieve yourself of some Russian caviar and French champagne. That is exactly what CNBC does every day of the week. They are constantly reminding investors of "what is working" or, in other words, "what you're missing" as the colour commentators (nee "book pumpers") hold centre stage.

I cite as a perfect example of the CNBC playbook the example of oil and gas stocks thus far in 2026.

All through the month of January, you could find nary a segment in which CNBC (or Bloomberg, for that matter) covered the energy names. If anyone mentioned Exxon or Haliburton, they were summarily dismissed as being "irrelevant" because a) no one cares and b) there were zero oil & gas advertisers filling CNBC's coffers (with vastly more emphasis on (b) than (a)). Then as suddenly as hypersonic missile hit U.S. bases in the Middle East, oil was at $120 with CNBC dusting off ancient Rolodexes to try to hunt down somebody — anybody — that could talk quasi-intelligently about energy.

This a classic example of why outlets like CNBC should be avoided like the Bubonic plague; they are 100% reactive and 0% predictive to market-impacting events. I hold out as evidence the case of gold-versus-Bitcoin in January. The precious metals have been outperforming Bitcoin for what seems like ages while in reality, the break started only last October. Yet despite this obvious outperformance by gold (and even greater using the gold mining stocks), CNBC continues to trot out crypto "experts" like Tom Lee hour after hour and day after day who constantly prattle on about "dollar cost averaging" and "long-term returns" whereas phrases like "crushing it" and "face-ripping rally" (in reference to owning Bitcoin) are now absent from the discussion. If I am able to listen to the CEO of Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE) or Newmont Corp. (NEM:NYSE; NGT:TSX; NEM:ASX) as much as once in the quarter let alone the month, it would go down in MSM history books.

So, it is now the second quarter of 2026 and the Middle East is ablaze while oil hums along at $112/bbl. The last time there as an oil shock anywhere close to this one it brought on a 25% drop in the S&P 500 against a 35% spike in oil. That was in 2022-2023 after the Russians made their move on the Ukraine followed by then-President Biden stealing their U.S. dollar reserves.

Fast forward to April 2026 and we have the mighty S&P 500 off a paltry 6% from its all-time high registered on January 28th at 7,002.28. Oil is up 105.5% in the same time period, an advance over three times the advance in 2021-2022.

Now retrograde to 1973-1974 with oil rising over eightfold due to the Arab Oil Embargo and consider the 41.9% drop during that oil-inspired bear market.

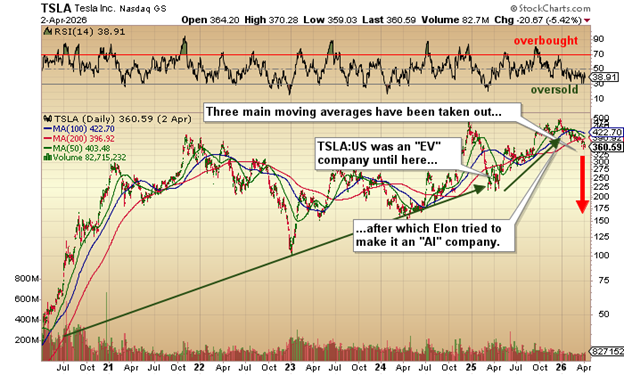

As an arbiter of global growth and economic health, I entitled this missive "Oil be back!" so as I am mulling over the tone and content of my current portfolio, I am forced kicking and screaming to look at the measly 6% feather-dusting of the S&P 500 against the sledgehammer pounding in 1973-1974 and wonder what happens to failed automakers like Tesla Inc. (TSLA:NASDAQ) when markets finally wake up. I am always drawn to statements repeated over and over ad nauseum from "legendary investor Warren Buffett" where he states that "you won't find out who is swimming naked until after the tide goes out" as an obvious allegory to finding out which companies are real and which companies are "phonies" only after the "irrational exuberance" vacates markets. TSLA:US has been riding the wave of cult-follower exuberance as those who view Elon Musk as the arrival of the next Messiah continue to bid up shares of his failed (and failing) EV manufacturer. On Thursday, I watched with glee as the company once again missed its number delivering 358,023 vehicles in Q1 2026, falling short of the analyst consensus of roughly 368,000 to 381,000 units. The company produced 408,386 vehicles, leaving a gap of more than 50,000 unsold cars added to its inventory. (Analysts view this "inventory build" as a sign of softening demand and a growing imbalance between supply and sales.)

CNBC has colour commentators continually chirping up the "Elon Effect" day after gruelling day resulting in regularly-scheduled short squeezes rescuing moving average trend lines and other technical support levels with mind-numbing frequency and predictability. However, on Thursday as the investing world headed into Good Friday and the Easter long weekend, markets punished Mr. Musk and the indestructability of his brand by slamming TSLA:US by 5.42% on the session making the YTD decline now 17.34%.

For me, TSLA:US represents everything I absolutely loathe about today's markets. This is a classic case of group manipulation where the government chooses a prodigal son (like Elon) and anoints him with anti-regulatory immunity and then holds him out as a shining example of American ingenuity and entrepreneurialism while he violates rule after rule while in total defiance of regulatory requirements and corporate governance.

Why?

It is because for all his faults, flaws, and foibles, Elon makes people money and a great deal of it. Because investors care not a whit as to the "how" (he makes his dough), they care only about the "how many", as in, dollars he puts in their pockets with his antics which have gone from the ridiculous to the sublime in recent months.

As a self-confessed bear on shares in TSLA:US (I own the T-Rex 2X's Inverse Tesla Daily Target ETF (TSLZ:US)), I have told subscribers that they should probably ignore my predilection for pain because I have ridden this ETF from $27 to under $10 and after averaging down (with great trepidation and ample doses of Jack Daniels and Percocet), I am now only mildly underwater but more optimistic today than I have been at ay time in the past year.

I have told subscribers that I own it "on principle alone" and that I will not cover until I watch TSLA:US break down through $100. Since it closed at $360.59, the funny sounds you are hearing out there are the shrieks of laughter from my subscriber base when they read that I am calling for "sub-$100" on the world's most overpriced automaker whose lunch is being heartily consumed by competitors BYD and Xiaomi (both Chinese).

As is always the case when this writer becomes obsessed with a whacked-out idea — caveat emptor.

Gold Price

Shifting to the metals, followers of this author will find it no surprise that I have been a stalwart bull on the gold market since launching the GGM Advisory back in 2020. I exited the senior and junior gold ETF's far too early in 2024 but remained long a basket of the junior gold and junior copper developers until last month when I bit the bullet hard (almost breaking two molars and one incisor) and bought June call options on both the GDX:US and the GDXJ:US, two ETF's that have over the years treated me lavishly.

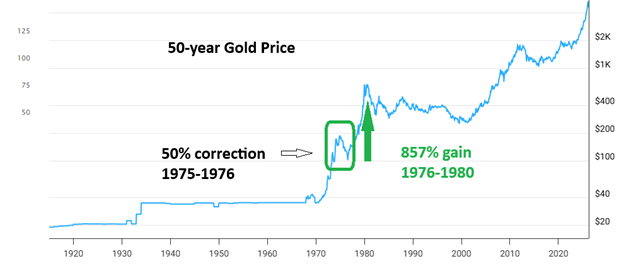

When asked why I would make such an insane move when it is so obvious that we have seen "generational highs" in both gold and silver in January, I responded by pointing to the chart of gold from 1920 until today, drawing reference to the mid-70's when a 50% correction took gold down from $190 to $100 in a couple of months before resuming its bullish configuration. Non-believers back then took handsome profits from the lows of $35 in 1971 by generating a 5.71 times return. However, if one bought the lows in 1976, they took a ride of 8.57 times their investment by 1980. I believe that the recent correction from $5,626 to $4,138 (∞ 25%) was enough to qualify as a "mid-course correction" in the journey to much higher prices.

I have never veered from my conviction that the 8,133 metric tonnes of gold allegedly held in trust by the Federal Reserve will be revalued in order to collateralize the massive (and growing) national debt estimated to be today approaching USD $40 trillion. Representing some 286 million ounces of gold, to fully back that debt with the U.S. gold reserve, the price would need to be pegged at USD at $139,860 per ounce. Now, perhaps a less-rabid figure of 10% of the national debt might be somewhat less "controversial" but even at that, it comes to $13,986 per ounce, a figure roughly three times the current price. As a comparative, when I launched the first Forecast Issue back in January 2020, the 10% figure was $8,741 per ounce with gold quoted at around USD $1,500 per ounce. The gold price required to back 10% of the current debt load has risen 600% in six years which is a sad and very disturbing testimonial to the state of America's balance sheet.

As a result, I started with the VanEck Senior Gold Miner ETF (GDX:US) putting out a "BUY" the weekend of March 20th and actually taking a position in the GDX June $75 calls at $10. I followed up later that week with the Van Eck Junior Miners ETF (GDXJ:US) June $115 calls at $10 while missing my entry level for the actual entry for the ETF's themselves.

The chart shown above was posted on Friday March 20th and you can see that the price action was indeed vintage "bottoming action" with RSI sub-30, and MACD and MFI plunging into deeply oversold territory at the time. That, coupled with the absolute delight by financial commentators the world over, spelled "BUY".

Longer-term, while the correction was shorter and of milder amplitude than 1976, I believe in principle that it was what was required in order to augment and extend the bull market that began in earnest on December 4th 2015 at $1,045 per ounce. Why do I know this? For the first time since the creation of CNBC in 1988, the "Cartoon Network" was covering gold and particularly silver every day on an hourly basis for the last two weeks in January while it was apparent that none of the anchors or colour commentators (except Guy Adami and Rick Santelli) owned as much as a sliver of either metal. That was the ultimate tip-off but the concrete confirmation came in the first few days of February when the entire CNBC newsroom was cheering at the crash in silver, failing to mention that even after the crash, silver was still outperforming the S&P by a fairly wide margin. Time, as they say, to "back up the truck", which I did.

As for the was in the Middle East, the markets listened to the boasting, bragging, bluster, and bravado of the American president on Wednesday evening and decided that it was not all as advertised because they took stocks apart on Thursday morning. However, as the day wore on, it became apparent to many that the American resolve is starting to flag as Trump told the world that "it will all be over in 2-3 weeks" so as markets are prone to do, they started to look out to a post-war scenario of weakening economies, higher inflation, fewer rate cuts and a burgeoning U.S. budget deficit and determined that what this virtually guaranteed, rather than a recession, was the arrival of the highly predictable fiscal stimulus that literally always materializes before the bear market cancer can metastasize.

For those bears out there, remember that lower economic activity during recessionary periods equals lower tax revenues and with the problem being faced by Treasury Secretary Scott Bessent, recession is not an option. Since stimulus equals more debasement, a lower dollar and higher commodities are in the cards and on the table. I reject the call for a return of the "Thundering Herd" once this stimulus arrives because we have been seeing this gradual but accelerating rotation out of tech (AI and Crypto) into hard assets since last fall. I see any new stimulus initiatives lighting a fire under the metals, food, and natural gas (which is cheap) rather than the ones that "worked" during the post-April lovefest last year...

Despite the longer-term bearish implications for stocks brought about by the oil spike, the short-term will be dominated by policy moves by the White House aimed at winning the November mid-terms and these policy moves will be centred around a rising stock market and global growth. The sacrificial lambs will be the U.S. dollar and long-term bonds which make it a breeding ground for the gold bugs, an environment well-covered by the GGM Advisory.

As you are sitting down for Easter dinner this weekend, remember that old and wonderful Irish prayer: "May I find myself in Heaven one hour before the Devil knows I'm dead."

Want to be the first to know about interesting Copper, Oil & Gas - Exploration & Production, Gold and Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter.

Subscribe

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Agnico Eagle Mines Ltd. and Tesla Inc.,

- Michael Ballanger: I, or members of my immediate household or family, own securities of: The Van Eck Junior Gold Miners ETF. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.