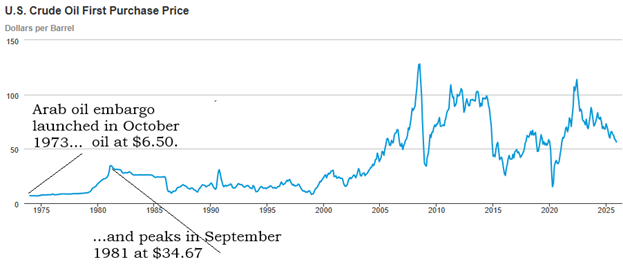

Back in March of 1981, the price of oil was trading at an astonishing $34.67 per barrel up from the lows of $6.67 in September of 1974 after the OPEC nations led by most of the Middle East oil producers that launched an embargo upon the United States for supporting Israel during the Yom Kippur War with US$$2.2 billion in aid.

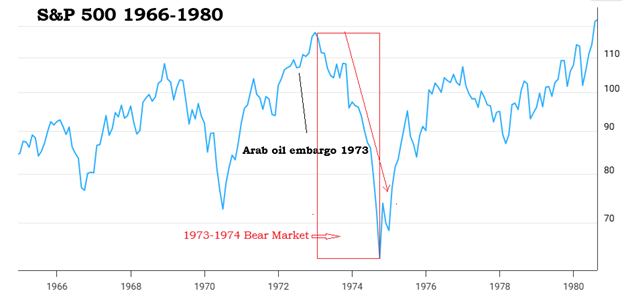

The S&P 500 fell 11.3% in the first month after the imposition of the embargo and accentuated the malaise of the equity markets which fell 48% from peak to trough during the same period.

Last weekend, the joint efforts of the Israeli and American armed forces launched an attack upon key military targets in Iran and while they are reported to have destroyed the majority of the country's leadership during the first wave of attacks, perhaps the most devastating unintended consequence was the response of the insurers who have basically told the shipping companies that anyone that passes through the Straits of Hormuz will be deemed "uninsured".

As a result, these immense oil and LNG tankers are huddled together on both sides of the Strait but staying well clear of anything that might appear threatening to the Iranian drones and gunboats that intend to close the waterway in order to once again punish the West for aiding and abetting the Israelis. As they say, history may not repeat but it can certainly rhyme".

Meanwhile, the Wall Street Spin Machine continues to spew out bullish tripe in ever-increasing volumes moving from the ridiculous to the sublime when they described this morning's NFP shocker (- 92k versus est. + 60k new jobs) as "bullish for bonds and therefore stocks" as the unemployment rate increased to 4.44% from 4.3%. Also praising the market's "resiliency", the spin merchants claimed that it was bullish that the S&P "only" dropped 1.33% today despite geopolitical drama, the poor jobs report, and surging oil prices all combining to instill fears of a 70-style stagflation.

However way you wish to spin it, there was a weekly close below the 20-week moving average for the S&P 500 which is important because it has remained above that m.a. since it broke out above it last May. Combining the weekly breakdown with the second consecutive daily close below the 100-dma and it sure looks like stocks are finally headed lower.

Also of note is the unemployment rate. The experts liken the "mindless passive bid" that emanates from the pension contributions of the average American worker that has been the progenitor of the endless "BUY" signal since around 2008 and with the growth of the liquidity pool since then, it has acted as a perpetual "dip-byer" and one that has consistently been "of last resort" constantly saving equities from anything more than a near term hiccup.

As the ranks of the employed dissipate and the ranks of the unemployed rise, that perpetual pool begins to shrink and along with it the size and frequency of the bids. Perhaps the explosion in the use of "AI" and the impending assault on white collar jobs is causing some erosion in the dependability of that "mindless and never-ending bid" that over time will be seen as the straw that broke the camel's back of stock market invulnerability. We shall see.

What has been surprising me concerning stocks has been the relative calm in the markets since last weekend. Every other geopolitical disturbance in the past twenty-six years has seen accelerated volatility enter the fray almost immediately but this time, traders seem to be so confident with Donald Trump's love affair with "stocks at all-time highs" as the ultimate scorecard for his legacy as president that they continue piling into the ETF's hand over fist on the assumption that as soon as stocks begin to cause pain, Trump will fire off a Tweet or call a press conference for the expressed purpose of rescuing stocks. No better evidence of that than the turn in April of last year when he earned the notoriety of the phrase "The TACO Trade" as in "Trump Always Chickens Out" when he revoked those egregious tariffs and then abandoned the draining of the Washington swamp after many of his Republican congressmen began to revolt as their political oxen (and re-election chances) were about to be gored.

From where I sit, stocks are two standard deviations above historical valuation levels which means that the S&P 500 is over-price, over-valued, and over-hyped by the media, the White House and the Wall Street spinmeisters remain desperate to keep the music playing despite the number of chairs being reduced by the hour. Having said that, I have been dead wrong in

doubting the current President. Whether or not you agree with his politics or his behaviour, he seems to have instilled a new swagger into the minds and hearts of Main Street America and as a Canadian that spent over six years living in various cities in that country, my friends in the Midwest seem to be relieved that finally someone is finally in the White house that a) cannot be "bought" and b) cares about the average working American. Perhaps that is what has been driving stock prices a good deal more than the outlook for corporate earnings. However, as recent polls would suggest, Trump's approval ratings are now as bad as they have ever been as many of the ethnic voting blocs are now returning to the Democrats which casts an ominous shadow on the mid-terms. If the Republicans lose the mid-terms to a ravenously angry Democratic left-wing mob, Wall Street will not like it any more than it does $90 oil and $5,150 gold.

Silver and Gold

Speaking of gold and silver, there is nothing I see from either a technical of fundamental basis in either of the two precious metals occurring this week that changes my near-term opinion: gold looks "great" and silver looks "not so great".

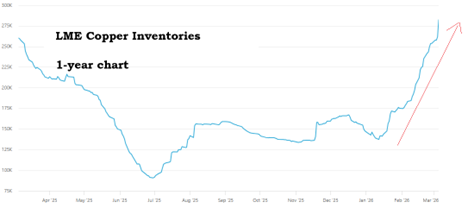

Copper appears to be chained to the global macro outlook but as much as the copper bulls like me love to point to the structural shortage conditions developing literally every week, inventory levels on the Shanghai, Comex, and London exchanges have been rising sharply since the start of the year.

Why should they not rise?

Chinese GDP data this week showed the slowest economic growth since 1991 so while the bulls keep chortling about "AI buildout" as a driver for copper demand, I might counter with "Chinese recession fears" as a counter-balance to that bullish narrative. This week's flair-up in the Middle East, if it follows the course laid out by the Qatari Energy Minister, could easily throw the global economy for a loop and no amount of "AI buildout" will offset the deflationary impact of global recession.

If stocks start to enter into a freefall, I can see the gold and silver miners being liquidated to shore up liquidity shortfalls with the same impact affecting the base metal miners as well.

I also think copper and silver prices could be impacted by the same drivers as the miners but I do not think gold will fare as badly because of the bullish leanings of the central bankers. I do not yet fear a broad market crash but if I did, gold would be where I would hide with natural gas a close second choice.

PDAC

The PDAC party ended on Wednesday at noon and I celebrated by driving my RAM 1500 Laramie for an hour and a half from lovely Port Perry to the Cambridge Suites Hotel in traffic-snarled downtown Toronto where I picked up Fitzroy Minerals Inc. (FTZ:TSX.V; FTZFF:OTCQB) Chairman Campbell Smyth, CEO Merlin Marr-Johnson and the jewel of the crew, country manager and COO Gilberto Schubert for a wonderful uptown dinner. Talking to the Chairman and CEO is quite easy because all of us were trained in the world of finance and while Merlin Marr-Johnson speaks three languages fluently (English, French, and Spanish), he also dabbles in six other languages and can at the very least communicate in all of them.

However, when it comes to conversing with Mr. Schubert whose native language is actually Brazilian Portuguese, it is especially challenging not from a linguistic perspective but rather from an intellectual perspective because Gilberto has three Master's degrees in Geology and when I am conversing with him, I am sure he finds it painful to have to talk down to me due to my limited knowledge of the topic in which he is a true master.

Not only is Gilberto a fine gentleman and an interesting participant in dinner conversation, he is impressive in all aspects f the world of mining from exploration to development to contract negotiation and domestic politics. As Chilean country manager for the Brazilian giant Vale Inc. for more than a decade, he knows every aspect of the Andean copper universe in the same way I know the world of junior mining. In fact, when you look across the table at this executive team of professionals, it is hard to imagine a more perfectly-aligned group along side to invest one's hard-earned capital. Chairman Campbell Smyth is the oil that keeps this finely-tuned machine functioning with such unique precision so when I think back to the 2020-2025 period when the juniors were imprisoned by walls of disinterest and ridicule, I thank my lucky stars that I made the decision to place a bet that for me was quite uncharacteristic.

You see, it has been five decades since I first felt the narcotic aura of the junior mining business when I plunked down my life savings in 1981 in a little junior "miner" (meaning a "shell company" with the word "Gold" as part of its name) only to discover five months later that the $.08 purchase of 20,000 shares ($1,600) had suddenly grown to $2.80 ($56,000). Matatchewan Consolidated Gold Mines was the first junior I ever bought and it was only after I began to conduct what I was later to refer to as "due diligence" that I learned that the only gold that would ever be associated with that company were the four letters contained in its name (G-O-L-D).

"There ain't no bull market like a GOLD bull market" is the old saw repeated in the wee hours of every PDAC party since its very creation back in 1932. The world has finally entered a perfect alignment of the planets here in 2026 as a topping stock market is giving way to a fledgling new

bull market in commodities led as always by gold and silver but now enjoined by oil and gas. If this follows the pattern of the 1970's, base metals and rare earth metals will soon join the festivities as the legions of cannabis, crypto, and "AI" speculators rotate away from the alluring world of paper assets into the intoxicating world of hard assets.

The Latin origin of the word "fiat" is derived from the phrase "let it be done". The reason paper money is referred to as "fiat" is that it finds its value in the exchange of goods and services "by government decree" rather than the backing of anything of value. Since governments have since the dawn of civilization elected to continually debase the purchasing power of the savings of its citizens, the world has finally awoken to that reality and are seeking out other safe havens for generational savings pools. It took a near meltdown in the fiat system in 2008 and a pandemic in 2020 to underscore the lawmakers' brazen disregard for the integrity of the world's reserve currency before the world actually woke up.

With the arrival of sobriety to the allocation of wealth, the junior mining and exploration sector has finally entered into a bona fide bull market and when measured in time as one would measure a baseball game, not only are we not in the "early innings", we have not yet heard the final bars of the "Star Spangled Banner".

By 2030, we should be experiencing the "Seventh Inning Stretch"…

| Want to be the first to know about interesting Silver, Oil & Gas - Exploration & Production, Copper and Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers, contractors, shareholders, and/or employees of Streetwise Reports LLC (including members of their household) own securities of Fitzroy Minerals.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: Fitzroy Minerals. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.