The Energy Report: Brian, is there a production cost for North American oil and gas producers at which most juniors can no longer afford to operate?

Brian Bagnell: When you're losing money—and at these prices, most companies are—the balance sheet becomes the most important asset you have. We have a number of producers that have balance sheets that are looking stretched on the current strip, but there are also a number that are doing fine, either through a combination of hedging in 2016 or conservative capital budgets in 2015 and 2016, which has left them in relatively good shape looking forward into 2016.

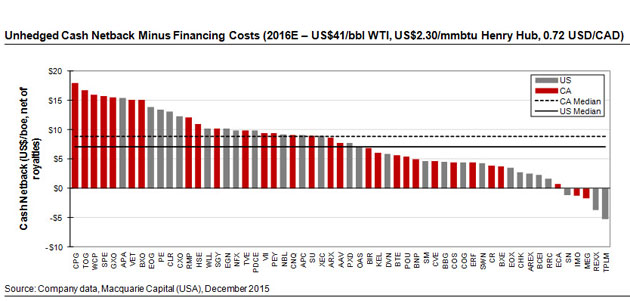

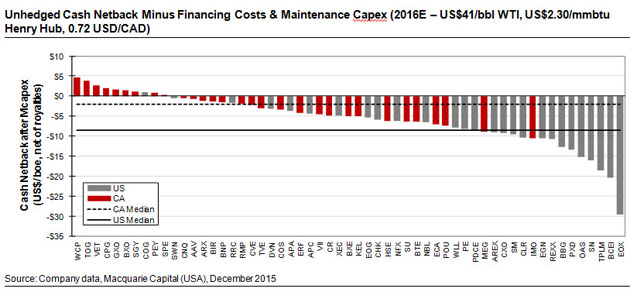

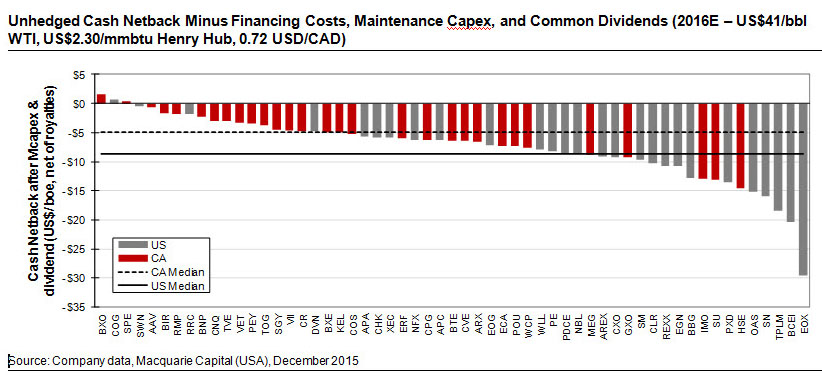

We did a study last month looking at break-even costs for all of our North American producers. We looked at 57 covered companies between Canada and the U.S. When the 2016 strip was hovering around $41 per barrel ($41/bbl), we found that the vast majority of companies were able to cover production costs. However, once you consider maintenance capital, which is money that needs to be spent by the company to hold production at current levels, only 9 out of 57 had excess cash flow. Once we factored in dividends, that number dipped to just three companies.

TER: How do you identify a junior company with staying power in this price environment?

BB: Again, the focus should be on the balance sheet because if a company is losing money the key plank to staying power will be its access to liquidity. So it just becomes a matter of how long a company is able to sustain this current downturn. The strength of the balance sheet is going to determine whether a company is able to hold on long enough to take part in a gradual increase in pricing.

TER: What will stabilize the market?

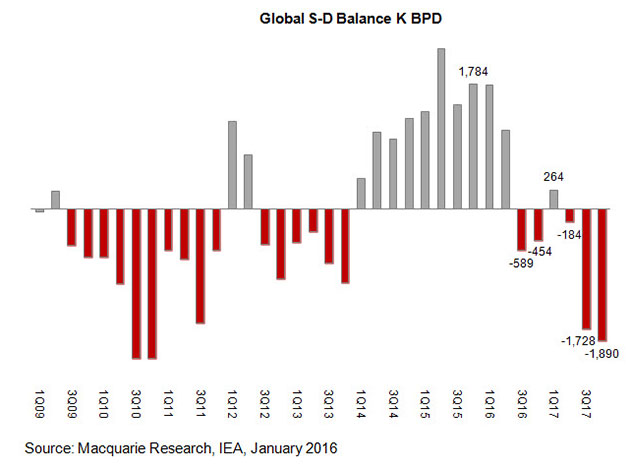

BB: It's a matter of supply coming offline. There are data points that help us to believe that demand for crude will continue to grow, but the key plank is going to be a reduction in supply. There are too many companies in the world right now losing money. Not all of them are going to make it. Not all of them are going to be able to sustain their current levels of production, which means production gets shut in or is allowed to decline. That also contributes to shrinking the gap between supply and demand. Our team thinks that the global supply/demand equation will start to come back into balance later this year.

TER: What would trigger a gradual price rise toward the end of this year?

BB: Aside from some event such as increasing tension in the Middle East or an emergency OPEC meeting resulting in an agreement to reduce production, it's just going to be a matter of supply declining or being shut in. It's not something that's going to happen all at once. It's going to be a slow response in companies shutting in wells or letting production decline.

TER: Are companies still shutting in?

BB: There hasn't been much shut-in activity in North America to date, even with the prices of crude where they are. You get into a bit of a tough situation with deciding to shut in production. If you shut in production, your cash flow will decline. As your cash flow declines, you're less able to maintain even a lower level of production and your costs per unit of production can increase. So it can become a bit of a downward spiral, though this is a bigger issue for companies with higher-than-average leverage.

"The royalty space is a reasonably safe place to hide in a low commodity price environment within the energy space."

We haven't seen much of that happen to date, although there is one event that I would point to that does give me cause for optimism: Whitecap Resources Inc. (WCP:TSX) recently announced that it would not be drilling any more wells through 2016. It has spent what it's going to spend on drilling for the year, and until prices improve, it doesn't see any reason why it should spend capital on wells that don't provide an adequate return. It is the first company to announce such a dramatic strategy. It is not a small company either. It has about 40,000 barrels of oil equivalent per day of production in Canada and has been a market darling. For a company like that to come out and make such an announcement took a lot of guts. It was the first mover. I think if we get enough companies that follow suit, that could help to get the market back in balance.

TER: How will that affect Whitecap's production?

BB: Its corporate decline rate is just north of 20%, so we could see production fall by about 20% over a year's time. This is fairly unique for the North American oil and gas space so far. Few other producers with strong balance sheets are allowing production to decline so materially. One of the benefits of doing that is its pro forma decline rate will be lower, which means that it will have to spend less capital to maintain a lower level of production, all else equal, which actually improves longer-term sustainability.

TER: What are oil and gas juniors doing now to retain and attract investors?

BB: Generally speaking, investors are very apprehensive about the energy space, especially about the junior space. Prices have fallen so far so fast that it will take quite a shot of confidence to get a lot of interest back into the sector. But as I said, balance sheet strength is top of mind for investors right now. There are certain companies that are able to offer some strength in that regard and are able to keep investors interested.

TER: What are the juniors doing to strengthen their balance sheets?

BB: Most of the companies with stronger balance sheets have them because of actions that they took when prices were higher and access to capital markets was there. Right now, very little is going on in the way of equity financings. Not a lot of investors are willing to put new capital to work in the junior oil and gas market. At the same time, banks are conducting reviews of credit facilities, and we have seen some companies announce reductions to those credit facilities, which makes access to capital even more challenging.

Some producers are trying to sell assets in an effort to strengthen their balance sheets, but commodity price volatility has been an impediment. So I'd say there is not a lot that they can do right now. They are where they are, and hopefully prices improve and confidence returns to the sector.

TER: Are you anticipating further mergers or bankruptcies in the sector?

BB: Absolutely. That will definitely accelerate in 2016 if prices stay around the current strip. We have seen some bankruptcies announced already since crude prices started diving. I think we will see merger and acquisition activity pick up as well, as the relatively strong acquire the relatively weak and make their own businesses stronger for the longer term.

TER: How deep will the price dive? As low as $20/bbl?

BB: I think anything could happen down here. We are at the margin at this point, and the price swings have been very wild. So it could happen. I just don't think it could stay there for any period of time because essentially nobody in the world would be making money at $20/bbl crude. That is just not sustainable.

TER: Let's take a look at some of the companies in your coverage universe. Why are you rating Advantage Oil and Gas Ltd. (AAV:TSX; AAV:NYSE) Outperform?

BB: Advantage has many of the characteristics that we just spoke about. The company has one of the better balance sheets in our North American coverage. The valuation is attractive relative to the North American space on strip pricing. It is still growing production and cash flow with internally generated cash flow. That means Advantage doesn't have to issue equity or take on new debt to grow production, even with current commodity prices. It was able to defer capital in 2016 to 2017 without affecting its growth plans in any material way. It's strong all around. On virtually every metric that we value Advantage on, it screens at the better end of our entire North American coverage.

TER: What is Advantage's hedging strategy?

BB: Advantage is hedged on roughly 52% of its net production in 2016 at prices higher than $3.50/thousand cubic feet, which is very, very attractive given that AECO prices are hovering at or below $2.25 today.

TER: Freehold Royalties Ltd. (FRU:TSX) has no employees or operations. It subsists on royalties alone. Why is it rated Outperform?

BB: The royalty space can be relatively strong in a sustained downturn. There could be opportunities for Freehold to acquire royalty packages from struggling producers in the oil and gas space. One potential source of financing for conventional exploration and production companies could be the sale of royalty assets. Some of those could be at attractive prices to Freehold in the current market.

On top of that, Freehold's balance sheet is relatively strong. It can sustain a dividend at far lower commodity prices than most nonroyalty producers just given that its costs are low and it doesn't have to spend much capital of its own. Freehold faces the same challenges that other royalty producers have resulting from lower drilling activity, but it's revised its capital and dividend plans down multiple times throughout the year to adjust to those challenges and avoid leaning on its balance sheet.

TER: Is Spartan Energy Corp. (SPE:TSX) prepared to weather the low price commodity storm? What is its strategy for the coming year?

BB: Spartan is relatively well positioned for low commodity prices. It has some of the lower supply costs of our North American producers. The wells it is drilling in southeast Saskatchewan are very cheap to drill and complete, and results have been tracking well above our regional type curves. As a result, it should have an easier time sustaining production than many of its peers. Spartan also has a pretty strong balance sheet on the current strip. It's one of the few producers that can maintain production in the $40/bbl WTI range without leaning on its balance sheet.

TER: How are the low prices affecting PrairieSky Royalty Ltd. (PSK:TSX)?

"The strength of the balance sheet is going to determine whether a company is able to hold on long enough to take part in a gradual increase in pricing."

BB: Drilling activity is down at least 50% in Western Canada over last year. Licensing activity, which is an indication of future drilling activity, is also down very materially. That is going to result in lower production on PrairieSky land, which results in lower cash flow. PrairieSky can do little to control that. It doesn't drill wells itself, so it's at the mercy of producers, though it does have some long-term drilling commitments that help protect it. While it does still have some pretty attractive land for development at the low end of the supply cost curve in Canada, royalties on PrairieSky's land are generally higher than they are on Crown land for similar prospects, which makes us think that it could have a hard time attracting capital in this environment. We think 2016 is going to be a challenging year. We think a dividend cut is quite likely coming up in February. It could be somewhere in the 30–40% range.

TER: Is that a greater dividend cut than other royalty companies are making?

BB: No. Freehold has already cut its dividend twice, whereas PrairieSky has not. It only sets its dividend policy once per year, so I would expect a cut in February. Its payout, which is a measurement of capital expenditures plus dividends divided by cash flow, is over 150% on strip pricing, which is higher than it should be for a company structured like PrairieSky. That said, it does have one of the stronger balance sheets in the Canadian oil and gas space, so people still see it as a name that provides some relative safety. We would agree with that. The royalty space is a reasonably safe place to hide in a low commodity price environment within the energy space.

TER: What is Toro Oil & Gas Ltd.'s (TOO:TSX.V) outlook for the coming year?

BB: It hasn't actually released a budget yet for 2016. It is still trying to decide how it will tackle the current environment. However, it has no debt right now, which gives it a position of relative strength in the junior market, although it will be trying to figure out the best way to finance a reduced capital program in 2016.

TER: Given all the unknowns and uncertainty, what would be your advice to investors in the junior oil and gas sector right now?

BB: Right now, the junior oil and gas market is facing a lot of stress. Your best strategy is to stick with companies that have better balance sheets that can withstand commodity prices staying at low levels through 2016 and can offer you upside when commodity prices start to improve. Stay away from the companies with the highest amounts of leverage just in case commodity prices stay lower for longer than you expect. Stick with the survivors. If you're looking to make a new investment in junior oil and gas markets, I would hold off until you see some signs of definitive improvement in the crude supply/demand balance that can give some visibility for sustained higher prices, because at $30/bbl WTI, it's very difficult for junior oil and gas companies to have any profitability.

TER: Thank you very much for taking the time to share your thoughts with us.

Brian Bagnell, CFA, is a research analyst in Canadian oil and gas company analysis for Macquarie Capital Markets in Calgary. He was formerly an investment associate at the NB Investment Management Corp. He holds a bachelor's degree in business administration (finance and accounting) from the University of New Brunswick.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Tom Armistead conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: None. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Brian Bagnell: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Spartan Energy Corp., Freehold Royalties Ltd., Whitecap Resources Inc. and Toro Oil & Gas Ltd. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.