When I looked over my notes this afternoon to attempt to find something — anything — about which to write that would not put readers to sleep, all I could conjure up was the resumption of hostilities in the Middle East.

However, there arose a deeper, darker story than the simple resurgence of missiles, drones, and aircraft assaults that revolved around the notion that U.S. equity markets are considered vital to the safety and security of the United States. You see, it is no secret that stock markets were heavily managed during World War II, with governments around the world taking extreme, unprecedented measures to control trading, prevent panic, and redirect all financial capital toward the war effort. Rather than letting free markets dictate prices, nations treated stock exchanges as strategic economic tools while setting hard price "floors" for blue-chip stocks from the onset of Pearl Harbor and beyond.

I mention this in passing because when the American-Israeli coalition first attacked Iran in late February, the price of oil shot through the roof. Prices immediately erupted into extreme volatility, and by the end of the first week of March, WTI surged over 38% to briefly cross $92 per barrel, while Brent crude jumped past $94 per barrel as the Iranian closure of the Strait of Hormuz severely choked off global energy shipments. However, after the specter of a crippling supply shock sent oil screaming further northward and stocks careening southward, a magical yet bizarre transformation came over the financial markets. Instead of geopolitical upheaval being a trigger for panic-buying of gold and silver, the two metals designed as hedges against calamity went in a diametrically opposite direction.

Each time the missiles took out a friendly target, stocks would rally, and the metals would fade. In fact, the gloomier the reports got for the U.S.-Israeli coalition, the worse gold and silver traded. The narrative for oil went from "$300 per barrel will be a cinch!" to "As soon as the peace deal arrives, oil will be back to $55," after which the traders began to short oil into every singular event that threatened supply. Instead of selling stocks due to the inflationary repercussions of $100 oil, traders were buying stocks, and instead of buying gold and silver, they were selling gold and silver. In the bizarro practice of protecting national security, east becomes west and up becomes down, and as they say, "never the twain shall meet".

The oddest behavior of any of those critical markets had to be crude oil prices. For the better part of four months, all we heard about was how strategic petroleum reserves were being drained unmercifully by the sovereign wealth funds that control them in order to prevent catastrophic drawdowns in domestic U.S. currency reserves. We were warned by the spin doctors at CNBC that "oil could see $500/bbl" once those SPR's were empty. While the narrative was being sculpted and scripted and shaped into something that the White House could accept, that "Great Peace Deal" that adds to the "Big Beautiful Bill" constituting the Trump legacy has metamorphosed into something drastically altered from what was being promoted back in March.

"Da Boyz" in the White House, along with their European and Asian allies, have kept the U.S. dollar sacrosanct in all aspects and character for one expressed purpose: to keep the illusion of "inflation under control" at the front and center of the American (and global) consciousness. Meanwhile, here in Canada, I just went to the local supermarket (non-operative word being "super") and filled a single carry-bag full of vegetables, including lettuce, celery, tomatoes, and cucumber for the ghoulish price of $100 (which of course did include a six-pack of Molson's beer).

I graduated from being a buyer of "cases of beer" perhaps thirty years ago. However, as muscle memory is a powerful tool, I recall all too well what it used to cost me fifty years ago for a "weekend up north" where I stuffed a "Two-Four" into the trunk of my 1976 Chrysler Cordoba ("with the fine Corinthian leather") and roared up the 400 highway. It was CA$7.25, so if you think for one Keynesian moment that inflation has been kept "under control" by our political leaders, you had better give your heads a firm and brain-adjusting shake. A case of Molson's Export beer is today priced at between $43 and $50 for twenty-four bottles of beer, not Napoleon Brandy or Madeira wine.

Chew on that for a while…

Gold and silver prices are rebounding off the lows registered at the end of the month, end of the quarter on June 30th. After thinking that the lows I identified on June 10 with RSI in the low 20's were a "false buy signal" resulting in a sale of everything I bought a week later, I was fortunate to have seen the error of my ways and decided that the lows were indeed in and replaced a silver long position represented by the SLV August $50 calls.

That trade was humming along swimmingly until the "Great Peace Deal" went up in smoke with a resumption of air assaults and the marine blockade. Gold had scrambled back to $4,200 and was well on its way to initial resistance at the downtrend line of $4,350 while the silver ETF (SLV:US), which bottomed just above $50, had rallied to just above $56 before hostilities resumed. Once the attacks on Iran resumed, the need for gold as a hedge against geopolitical risk was jettisoned, and the selling resumed. The good news is that the end-of-quarter lows are holding, at least as of Friday, with both gold and silver taking their lead from oil, which has not spiked back anywhere near $120, where it topped last March.

Followers of this publication should know that while I am a fervent bull on precious metals on a secular basis, I believe we are now in a cyclical bear market with more downside risk until gold tops $4,900 and silver tops $100. Down nearly 30% year-to-date, if gold can close above that downtrend line at $4,350, it stands a good chance of testing the 100-dma at $4,613. SLV:US needs a nudge above $54 after which it should (there's that operative word again) track to the 100-dma at $67.35. That is a great trade from $50 where I entered the calls, but it is only that if the metals can ignore the war drums and oil's leading indicator status and forge ahead, driven by accelerating demand and improving money flow. The "money flow indicator" ("MFI") for the gold ETF (GLD:US) turned up in March despite weaker prices and is now trending UP, which is bullish.

The bulls look to a global structural shortage of silver arriving over the next year, triggered by a massive increase in consumption. They point to surging demand from green energy (solar panels), electric vehicles, semiconductors, and artificial intelligence infrastructure (AI data centers). Notable silver bulls include Eric Sprott, who highlights "next-generation solid-state batteries (like Samsung's 900km-range battery) which require up to a kilogram of silver per unit." He notes that "if these are commercialized widely, they could consume nearly the entire global annual silver supply".

The problem I have is that the bull case for silver and all of the accompanying bullet points that are rhymed off by these high-profile gurus is exactly what drove it to $123 back in January, yet prices are now down over 50% in five short months.

These bullish arguments have not changed one iota since the January 29th peak but price most certainly has been rendering the future "uncertain at best". Without argument, silver may need a new catalyst to resume the assault on the old highs and thus far, all I hear is the same narrative recanted with the same fervor from all the same notables and if history has taught us one valuable lesson, it is that bullish narratives slowly fade into the sunset based solely on price and not upon repetition of the same old story.

For these reasons, I am a short-term bull on silver, but make no mistake; I am a "renter" rather than an "owner" of this position in silver. While the secular case has not changed, there needs to be a world of technical reparations in both gold and silver before the "All Clear!" signal is sounded.

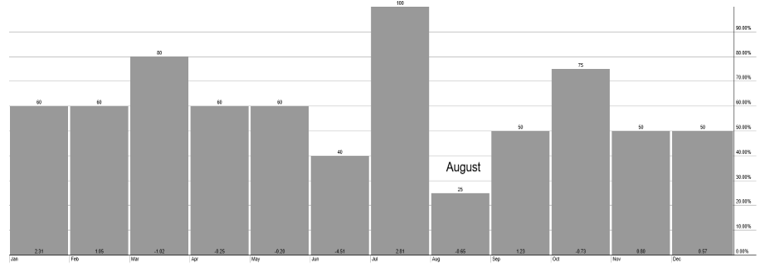

The junior miners are doing to investors what they always do in the months of June through September: they are driving them to serial depression and aggravated angst. I rarely put out "sell" recommendations on issues I own until they have given me good reason to do so. I normally give company management the benefit of the doubt and enough time (and rope) to either succeed or hang themselves, but what I never do is put out a "sell" in March on 50% of all positions in advance of PDAC and the arrival of summer. Every single year, as far back as I can recall, I have made reference to the seasonality of the junior miners and how the best buying opportunity for the juniors is usually the last two weeks of August. The chart shown below is the seasonality chart for the S&P/TSX Venture Index, showing how August is perennially the weakest month of the calendar year for the junior mining sector.

Despite my haranguing all through March and April over the fact that junior miners are heavily dependent upon drill results, the expectation of favorable drilling outcomes is always what keeps me from issuing "sells," and that has been a definite drawback, particularly in 2026. Last year, the summer doldrums were far less impactful and in fact unnoticeable because the months of June through September had gold, silver, and copper in clearly-defined uptrends about to enter the final "vertical" stage of ascent, which they did in unison in January of the following year.

The current summer of 2026 is markedly different than last summer because Wall Street has done masterfully what Wall Street always does masterfully, and that is sculpt the investor narrative away from anything benefiting from inflation and toward anything benefiting from technology, which they argue enhances productivity and therefore advances the "human condition" with disinflationary repercussions.

Whereas last January money was flowing with reckless abandon toward the "dollar debasement trade" otherwise known as the "hard assets trade", the Wall Street gang, riddled with envy, determined that they needed their own moonshot "story" where they could control prices (and charge fees) to replace the silver trade where they could not control prices and could not charge fees. So, what did they do? They conjured up the "AI" trade and replaced silver with the semiconductors; only the move in the semiconductors has absolutely dwarfed the move in silver in terms of total money flow and fees charged. The fees on the Spacex IPO were over $850 million spread out among some two-hundred companies which now has the moneychangers in New York focused 100% on "the next Spacex" and not to any large degree in the hunt for "the next silver deal" because the entire value of global silver dollar volume is simply too miniscule to facilitate the fee structure required by the Wall Street generals.

So the junior mining investors are forced to sit back and watch the CNBC "colour commentators" squawk about how filthy rich Elon Musk is or how filthy rich Sam Altman is about to become while the entire group of "AI" companies buy each others products and each other's stock as they keep the largest Ponzi scheme in history alive and bubbling all on the pretense that the West is in a "Race for AI Supremacy" with the Chinese, the winner of which will be rewarded with global hegemony and reserve currency status for life.

Lost in the shuffle are all of the bullish bullet points that drove the U.S. dollar index to 95.5, where the exact low for that currency coincided perfectly with the blow-off tops in gold and silver the same day, January 29, 2026. I get dozens of emails and DM's asking me why the national debt at nearly USD $39 trillion has not yet caused a run on the dollar and a crash in both U.S. treasuries and stocks, and I am at a loss to provide anything that might be construed as "sound advice". The only answer that seems plausible is the fact that the U.S. financial markets have been "the goose that keeps on giving" and as such, have been the one place where investors the world over have continually made money, and particularly in recent months, a great deal of money, especially in the semiconductors. The old expression — that "money gravitates to where it is treated best" — most certainly applies to the U.S. technology and U.S stocks in general. Once that becomes a thing of the past and the major U.S. markets roll over, taking the U.S. dollar back into its long-term downtrend, money will once again seek out sectors that are treating them "best", just as were the gold, silver, and copper juniors last year.

In the interim, I am taking off on a tour of the Danube River next week while doing my best to ignore the bid-ask on my fully-funded junior miners, which have remained flat-to-down for most of the past six months despite some great news releases. I desperately want to see "September 1, 2026" on the calendar, and since staring at my phone or watch does nothing to hasten that event, I need to get my mind off these agonizing summer doldrums that happen every single year, leaving me scratching my head as to why every year I fail to lighten up when the ducks are all quacking in February.

As a final punctuation mark on the juniors, we all must come to the realization that the Wall Street generals know all too well that their sitting president is a huge fan of the capital markets, whether it be trading tech stocks or launching his own cryptocurrency. With a "stockroach" scurrying around the White House, the New York gang that controls markets will never let the bull die without one whale of a battle. Too much money is being made promoting and promulgating the bull market narrative for them to gracefully cede control until it is no longer profitable to do so. Remember this: They will never ring a bell when it is time to leave the Wall Street party. Bear markets arrive like a thief in the night; you wake up in the morning, and all your valuables are gone.

It may just be that the juniors will need to wait until the love affair with U.S. "AI" is over before they are able to treat money well. Events that underscore the current mania for the "AI" sector include the recent listing of SK Hynix Inc. (HKHYV:US), the largest-ever U.S. market debut by a non-American company. The South Korean semiconductor giant raised $26.5 billion by issuing American Depositary Receipts (ADRs) at $149 each, vaulting its market cap to approximately $1 trillion. When the junior miners once again begin to treat investors as well as these types of transactions have, all of the bullish bullet points for gold, silver, and copper miners will once again be current and will celebrate a return of the narrative that sent gold to $5,626, silver to $124.45, and copper to $6.78/lb.

| Want to be the first to know about interesting Gold, Copper, Oil & Gas - Exploration & Production and Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Michael Ballanger: I, or members of my immediate household or family, own securities of: silver ETF (SLV). My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.